Introduction: The Gen Z Revolution in Life Insurance Trends

Picture this: A 25-year-old software developer sits in a coffee shop, scrolling through TikTok on her lunch break. Between recipe videos and travel content, she stumbles upon a financial influencer explaining life insurance. But here’s the twist—they’re not talking about what happens after you die. They’re explaining how life insurance can protect you right now, while you’re living, breathing, and building your future.

This is the new reality of life insurance trends in 2026, and it’s being driven by the most misunderstood generation in the workforce: Gen Z.

For decades, the life insurance industry operated on a simple premise: you pay premiums throughout your life, and when you die, your beneficiaries receive a payout. It was straightforward, predictable, and—let’s be honest—pretty depressing to think about. But Gen Z is flipping this age-old model on its head, demanding something radical: insurance that actually benefits them while they’re alive to enjoy it.

According to the World Life Insurance Report 2026, a groundbreaking study by Capgemini and LIMRA, 68% of adults under 40 recognize life insurance as essential for financial health. Yet traditional offerings don’t align with their priorities, creating a massive disconnect between what insurers sell and what younger consumers actually want. The report reveals that Gen Z and millennials are seeking near-term benefits they can access throughout their lives—not just a death benefit their families receive decades from now.

The shift is so profound that it’s forcing the entire life insurance industry to rethink its century-old business model. Welcome to the era of “living” coverage, where modern life insurance is as much about protecting your present as securing your family’s future.

Understanding Living Benefits Insurance: What Gen Z Really Wants

The Fundamental Difference: Life Insurance vs Traditional Death Benefit

Before we dive into why Gen Z is rejecting traditional approaches, let’s clarify what we mean by living benefits insurance versus traditional death benefit policies.

Traditional Death Benefit Life Insurance:

- Pays out only upon the policyholder’s death

- Beneficiaries receive a lump sum to cover final expenses, debts, lost income

- Primary focus: financial protection for surviving family members

- Value realized: decades in the future, often 40-50 years after purchase

- Mindset: preparing for the worst-case scenario

Modern Life Insurance with Living Benefits:

- Provides access to death benefits while you’re still alive under certain conditions

- Includes accelerated death benefit riders for critical, chronic, or terminal illness

- Offers wellness rewards, health incentives, and preventive care support

- May include cash value accumulation you can borrow against

- Primary focus: financial security throughout your entire life journey

- Value realized: potentially within months or years of purchase

- Mindset: building confidence and optionality for life’s unpredictable moments

The distinction isn’t just semantic—it represents a fundamental philosophical shift in how we think about insurance. Gen Z doesn’t want to simply plan for death; they want protection that adapts to the actual challenges they’ll face while building their lives.

What Are Living Benefits? A Comprehensive Breakdown

Living benefits, also known as accelerated death benefit riders, allow policyholders to access a portion of their death benefit before they die if they meet specific qualifying conditions. Here’s what modern life insurance living benefits typically include:

Critical Illness Coverage: Access your death benefit if diagnosed with serious conditions such as:

- Heart attack or stroke

- Invasive cancer

- Major organ transplant

- Kidney failure

- Paralysis

- ALS (Amyotrophic Lateral Sclerosis)

- Severe burns

- Arterial aneurysms

Chronic Illness Coverage: Activate benefits if you’re certified as unable to perform at least two “activities of daily living” (ADLs) for 90+ days, including:

- Bathing

- Eating

- Dressing

- Toileting

- Transferring (changing positions)

- Continence (bladder/bowel control)

Or if you require substantial supervision due to cognitive impairment like Alzheimer’s or dementia.

Terminal Illness Coverage: Access benefits if a physician certifies you have an illness expected to result in death within 24 months.

Additional Modern Features Gen Z Values:

- Wellness rewards for healthy behaviors (gym memberships, preventive care)

- Mental health support and counseling services

- Fertility treatment coverage

- Maternity and paternity support

- Financial planning and budgeting tools

- Telemedicine access

- Prescription discount programs

Many insurers now include these living benefits at no additional cost, recognizing that they attract younger customers who view insurance as a holistic financial planning tool rather than just a death benefit.

Shocking Reason 1: Gen Z Insurance Priorities Focus on Immediate, Tangible Value

The “Show Me Now” Generation

Gen Z grew up in a world of instant gratification. They can stream any movie immediately, order food with a tap, and video chat with friends across the globe in seconds. This instant-access mindset extends to their financial products—and traditional life insurance’s “you’ll appreciate this in 50 years” value proposition simply doesn’t resonate.

The Capgemini-LIMRA report found that 25% of under-40 consumers cite “lack of immediate benefits” as a barrier to purchasing life insurance. Another 32% say coverage doesn’t align with their current life stage. These aren’t objections to be dismissed; they’re fundamental insights into how Gen Z insurance buyers think about value.

Why Traditional Death Benefits Feel Abstract and Distant

Consider the typical Gen Z financial reality in 2026:

- Average age of first-time homebuyers: 36 years old (up from 29 in previous generations)

- Percentage planning marriage in near term: Only 37% of adults under 40

- Percentage planning children soon: Just 16% of under-40s have immediate plans

- Student loan debt: Average of $28,950 per borrower

- Living with parents: 31% of 25-34 year-olds still live with family

When you’re 24, drowning in student debt, working a contract job with no benefits, and years away from marriage or homeownership, the idea of paying monthly premiums for a benefit that only activates when you die feels… irrelevant. It’s not that Gen Z doesn’t understand mortality or responsibility—it’s that traditional life insurance offers zero tangible value for their current, very real challenges.

The Living Benefits Solution: Coverage That Grows With You

Modern life insurance with living benefits changes the calculation entirely. Suddenly, that monthly premium isn’t just for some distant, abstract future. It’s protection against:

- The critical illness that could bankrupt you in your 30s

- The chronic condition that might require long-term care

- The unexpected health crisis that could derail your career

- The mental health support you might need during stressful periods

- The wellness programs that keep you healthy and reduce other healthcare costs

As one Gen Z policyholder explained on a recent financial wellness forum: “I got life insurance at 26 not because I think I’m going to die young, but because I know people our age who’ve faced cancer, serious accidents, and chronic illnesses. The living benefits mean if something happens, I can access money to focus on recovery without destroying my finances. That’s worth way more to me than just knowing my parents would get a check if I died.”

The Data Behind the Demand

According to research from LIMRA and Life Happens, 49% of millennials and 47% of Gen Z say they need life insurance or more of it. But when asked what would make them more likely to purchase, the top factors weren’t about death benefits—they were about accessible, flexible features that provide value throughout their lives.

The Corebridge Financial study found that 46% of millennials and 40% of Gen Z would be more likely to buy a policy if it could be approved within 24 hours—but approval speed is only part of the equation. They also want products that address their actual life stage: career building, debt management, health optimization, and financial flexibility.

Shocking Reason 2: How Gen Z Is Changing the Life Insurance Industry Through Digital-First Expectations

The Technology Gap That’s Costing Insurers Billions

Here’s a jaw-dropping statistic from the Capgemini research: 59% of under-40s want direct digital engagement with their life insurance, but only 31% of insurers actually offer the platforms to enable it. Even more striking, 77% of consumers expect comprehensive, data-driven recommendations, but just 16% of insurers provide them at scale.

This isn’t a minor preference—it’s a fundamental mismatch between how Gen Z lives their lives and how the insurance industry operates. And it’s costing insurers access to the most valuable demographic segment: young, healthy individuals who could be customers for the next 50+ years.

The Old Way: Agents, Applications, and Anxiety

Traditional life insurance purchasing looked like this:

- Schedule an appointment with an insurance agent (during business hours)

- Sit through a 90-minute presentation about mortality tables and premium structures

- Fill out extensive paper applications with confusing medical history questions

- Schedule a medical exam at a testing facility

- Wait 4-6 weeks for underwriting review

- Exchange multiple phone calls and emails to clarify information

- Finally receive approval and policy documents

- Never really understand what you bought or how to use it

For Gen Z, this process feels archaic, opaque, and unnecessarily complicated. It’s insurance designed for a world where people had single careers, stayed in one location, and planned major life milestones in their 20s.

The New Way: Digital, Transparent, Instant

Modern life insurance platforms have revolutionized the experience:

- Online quotes in minutes: Input basic information and see personalized rates instantly

- Simplified underwriting: Many policies require no medical exam for healthy applicants

- 24-hour approval: Nearly half of Gen Z says same-day approval would increase their likelihood of purchasing

- Mobile-first applications: Complete the entire process on your smartphone

- Transparent pricing: Clear explanations of what you’re paying for and why

- Digital policy management: View coverage, file claims, and adjust policies through apps

- Educational content: Video explainers, calculators, and comparison tools

- Instant customer service: Chatbots and live support available 24/7

Insurtech companies like Ladder, Haven Life, Bestow, and Ethos have built their entire business models around this digital-first approach—and traditional insurers are racing to catch up or risk losing an entire generation of customers.

Social Media as the New Insurance Advisor

Perhaps the most dramatic shift: Gen Z learns about life insurance primarily through social media, not through traditional agents or advertising. According to research, about two-thirds of those aged 18-42 use YouTube for financial information, followed by Instagram, Facebook, and TikTok.

Financial influencers on these platforms are reframing life insurance conversations:

- Breaking down complex concepts into 60-second videos

- Sharing personal stories of how living benefits helped during illness

- Comparing policies side-by-side with clear pros and cons

- Debunking myths about cost and complexity

- Making insurance feel accessible rather than intimidating

This represents a fundamental power shift. Information that was once controlled by agents and companies is now democratized, putting Gen Z in control of their research and decision-making process.

The Consequence: Adapt or Become Obsolete

Insurance companies face a stark choice: modernize their product design, simplify purchase paths, and create digital experiences that feel human and helpful—or watch Gen Z purchase coverage from tech-forward competitors who were built for this moment.

The companies winning with Gen Z share common characteristics:

- Mobile-optimized everything

- Radical transparency about pricing and coverage

- Living benefits as standard features, not expensive add-ons

- Gamified wellness programs that reward healthy behaviors

- Seamless integration with other financial apps and tools

- Educational content that empowers rather than confuses

Shocking Reason 3: The Gig Economy Made Traditional Death Benefits Insufficient

The End of Employer-Provided Everything

Previous generations followed a relatively standard path: graduate, get hired at a company, receive a benefits package including group life insurance, stay for 30 years, retire with a pension. Life insurance was often something your employer provided, not something you actively purchased.

Gen Z’s work reality couldn’t be more different:

- Job-hopping frequency: The average Gen Z worker will have 10+ different employers by age 34

- Gig economy participation: 32% of Gen Z workers have a side hustle or freelance income

- Contract work prevalence: 27% work as independent contractors without traditional benefits

- Remote work expectations: 74% prefer or expect remote work options

- Entrepreneurship aspirations: 62% of Gen Z wants to start their own business

When you’re piecing together income from Uber driving, freelance design work, and a part-time retail job, guess what you don’t have? Employer-provided life insurance. Or health insurance. Or disability coverage. Or really any benefits at all.

The Protection Gap Nobody Talks About

This employment shift has created a massive insurance gap. Freelancers, contractors, and gig workers must secure their own coverage—but traditional life insurance products weren’t designed for their unstable income patterns, lack of medical benefits, or uncertain career trajectories.

Enter modern life insurance with living benefits. These policies address the gig economy reality:

Income Flexibility:

- No employer required for coverage

- Premium payment flexibility for variable income

- Ability to adjust coverage as earnings fluctuate

- Portable protection that moves with you between jobs

Comprehensive Protection:

- Living benefits that replace the safety net employer benefits used to provide

- Critical illness coverage when you don’t have employer disability insurance

- Chronic illness protection when you’re responsible for your own long-term care

- Health and wellness support when you lack employer health programs

Business Protection:

- Coverage that protects your entrepreneurial ventures

- Policies that can fund buy-sell agreements for business partners

- Protection for business loans and obligations

- Income replacement if illness prevents you from working

Real-World Example: The Freelancer’s Safety Net

Consider Maya, a 28-year-old freelance graphic designer. She has no employer, no benefits package, and income that varies between $3,000 and $7,000 monthly. Traditional life insurance felt pointless—she has no spouse or children, and her parents are financially stable.

But when she discovered modern life insurance with living benefits, the value proposition changed completely:

- If she’s diagnosed with cancer, she can access $100,000 to cover treatment while focusing on recovery instead of hustling for client work while sick

- If she develops a chronic condition requiring long-term care, she has financial protection without employer disability insurance

- If she’s in an accident and can’t work for six months, living benefits provide a financial cushion

- The wellness rewards program gives her discounts on gym memberships and preventive care she’d otherwise skip to save money

- If she does eventually have children, the death benefit protects them too

Suddenly, life insurance isn’t just about death—it’s about financial security across all the scenarios her precarious work situation makes more risky.

The Industry Response: Flexible Products for Flexible Lives

Forward-thinking insurers are redesigning products specifically for gig economy workers:

- Modular coverage: Add or reduce coverage as your income and needs change

- Pause options: Temporarily reduce premiums during lean months

- Multi-benefit policies: Combine life, disability, and critical illness in one package

- Business-friendly features: Options specifically designed for entrepreneurs and self-employed individuals

- Affordable entry points: Low minimum coverage amounts to accommodate variable budgets

These innovations directly address why Gen Z is changing the life insurance industry—they’re demanding products that fit their actual lives, not the standardized career paths of their grandparents’ generation.

Shocking Reason 4: Financial Trauma and Uncertainty Drive Demand for Living Benefits Insurance

The Formative Experience of Economic Crisis

Gen Z’s financial worldview was shaped by events previous generations never experienced at such formative ages:

2008 Financial Crisis: The oldest Gen Zers were teenagers when they watched their parents lose jobs, homes, and retirement savings. They saw “stable” careers evaporate overnight and retirement plans destroyed.

COVID-19 Pandemic: Just as Gen Z entered the workforce, a global pandemic shut down entire industries, eliminated millions of jobs, and demonstrated how quickly “normal” can collapse. One in seven Gen Zers are now maxed out on their credit cards, and delinquencies among young adults are rising.

Student Debt Crisis: Gen Z graduated into the most expensive education market in history, often carrying debt equivalent to a small mortgage before earning their first real paycheck.

Housing Unaffordability: Median home prices relative to median incomes are at historic highs, making homeownership feel impossible for many young adults.

Healthcare Costs: Medical bankruptcy remains a leading cause of financial ruin, even for insured individuals.

These aren’t abstract statistics—they’re lived experiences that fundamentally changed how Gen Z thinks about financial security and risk.

The “Expect the Unexpected” Mindset

Unlike previous generations who could reasonably plan for stable careers and predictable life milestones, Gen Z operates with a baseline assumption that life is fundamentally unpredictable. They’ve watched economic security evaporate repeatedly and learned that preparation matters more than optimism.

This mindset makes living benefits insurance incredibly appealing. It’s not just about protecting against death—it’s about having a financial safety net for the inevitable unexpected challenges life will throw at them.

As the Bankrate research noted, one Gen Z couple explained their decision to purchase life insurance before having children: “We were both young and healthy at 28 and 29 years old… After we had our daughter, there was no question. We went for the highest payout option possible, so if one of us passed, the other could focus on her and not have to worry about paying off the house, affording groceries, etc.”

This proactive approach—securing coverage before needing it, preparing for scenarios they hope never happen—reflects Gen Z’s financial trauma-informed decision-making.

Living Benefits as Financial Resilience

For Gen Z, modern life insurance with living benefits represents more than insurance—it’s a resilience strategy:

Protection Against Medical Bankruptcy: Critical illness coverage means a cancer diagnosis won’t destroy everything you’ve built. Instead of choosing between aggressive treatment and financial survival, living benefits provide the resources to pursue both.

Career Flexibility Buffer: Knowing you have chronic illness coverage creates freedom to take career risks, start businesses, or pursue meaningful work rather than just chasing employer benefits.

Mental Health Security: The stress of financial vulnerability takes a tremendous toll. Having comprehensive protection—including living benefits—reduces anxiety and allows Gen Z to focus on building their lives rather than constantly worrying about worst-case scenarios.

Generational Wealth Building: For Gen Z individuals who are first-generation wealth builders, insurance with living benefits protects the financial progress they’re making. One serious illness won’t undo years of hard work.

Shocking Reason 5: Gen Z Values Wellness, Prevention, and Quality of Life Over Pure Financial Products

The Wellness Revolution Meets Insurance

Gen Z is the most health-conscious generation in modern history. They prioritize:

- Mental health and therapy

- Preventive care and early intervention

- Fitness and physical wellness

- Nutrition and clean eating

- Work-life balance and stress reduction

- Holistic health approaches

Traditional life insurance ignored all of this. It was a purely financial transaction: pay premiums, die eventually, beneficiaries get money. There was no connection to actually living healthier, preventing disease, or improving quality of life.

Modern life insurance is changing this paradigm by embedding wellness into the insurance experience itself.

Gamification and Rewards for Healthy Behaviors

Leading insurers are now offering:

Activity Tracking Rewards:

- Connect your Fitbit or Apple Watch

- Earn points for daily step goals

- Get premium discounts for consistent exercise

- Receive bonuses for completing fitness challenges

Preventive Care Incentives:

- Discounts for annual physicals and health screenings

- Rewards for completing recommended vaccinations

- Bonuses for maintaining healthy BMI, blood pressure, cholesterol

- Credits for participating in wellness coaching programs

Mental Health Support:

- Access to meditation and stress management apps

- Teletherapy sessions included or discounted

- Mental health crisis support hotlines

- Wellness check-ins and proactive outreach

Lifestyle Benefits:

- Gym membership discounts or reimbursements

- Healthy meal delivery service partnerships

- Smoking cessation program support

- Sleep tracking and improvement resources

From Insurance Company to Life Partner

This shift transforms the relationship between insurer and policyholder. Instead of an impersonal corporation you pay monthly and hope to never interact with, modern insurers position themselves as partners in your lifelong wellness journey.

The value proposition becomes: “We’re not just protecting you if something goes wrong—we’re actively helping you stay healthy and live better.”

For Gen Z, this resonates powerfully. They don’t just want products; they want brands and companies that align with their values and support their goals. An insurer that helps them stay healthy, provides mental health resources, rewards positive behaviors, and offers living benefits when illness strikes is far more appealing than one that simply waits for them to die.

The Fertility and Family Planning Connection

Another area where modern life insurance addresses Gen Z priorities: fertility and family planning support. Some policies now include:

- Coverage for fertility treatments and IVF

- Maternity and paternity leave income support

- Adoption assistance benefits

- Family planning counseling and resources

Traditional life insurance assumed you’d have children naturally and on a standard timeline. Modern living benefits insurance recognizes that Gen Z’s path to parenthood is often more complex, expensive, and uncertain—and provides support throughout that journey.

Comparing Traditional vs. Modern Life Insurance: What Gen Z Actually Gets

To clearly illustrate the difference between traditional death benefit focus and modern living benefits approach, here’s a comprehensive comparison:

| Feature | Traditional Life Insurance | Modern Life Insurance with Living Benefits | Why Gen Z Prefers Modern |

|---|---|---|---|

| Primary Purpose | Death benefit for beneficiaries | Comprehensive life protection including living benefits | Want protection for scenarios they’ll actually face |

| When Benefits Activate | Only upon death | Critical illness, chronic illness, terminal illness, plus death | Access to funds when they need help most |

| Value Timing | 30-50 years in the future | Potentially within months or years | Immediate, tangible value proposition |

| Wellness Integration | None | Fitness tracking, preventive care rewards, mental health support | Aligns with health-conscious values |

| Application Process | Lengthy forms, medical exams, weeks of waiting | Digital applications, simplified underwriting, 24-hour approval | Matches expectations for convenience |

| Policy Management | Paper documents, phone calls, in-person meetings | Mobile apps, online portals, instant customer service | Digital-native experience |

| Coverage Flexibility | Fixed coverage, difficult to modify | Modular design, adjustable as life changes | Adapts to gig economy reality |

| Target Life Stage | Married with children, homeowners | All adults regardless of marital/parental status | Relevant at any life stage |

| Educational Resources | Agent-dependent, limited materials | Video tutorials, calculators, transparent comparisons | Self-directed research preference |

| Cost Transparency | Opaque pricing, hard to compare | Clear breakdown of costs and coverage | Demand for transparency |

| Additional Features | Basic death benefit only | May include fertility support, business protection, career transition help | Addresses actual Gen Z challenges |

| Typical Monthly Premium (Healthy 25-year-old, $250K coverage) | $15-25 term life | $20-35 with living benefits | Willing to pay slightly more for comprehensive protection |

| Approval Requirements | Extensive medical history, often requires exam | Simplified questions, many require no exam | Removes barriers to purchase |

| Cultural Messaging | “Protect your family after you’re gone” | “Protect yourself and your future throughout life” | Less morbid, more empowering |

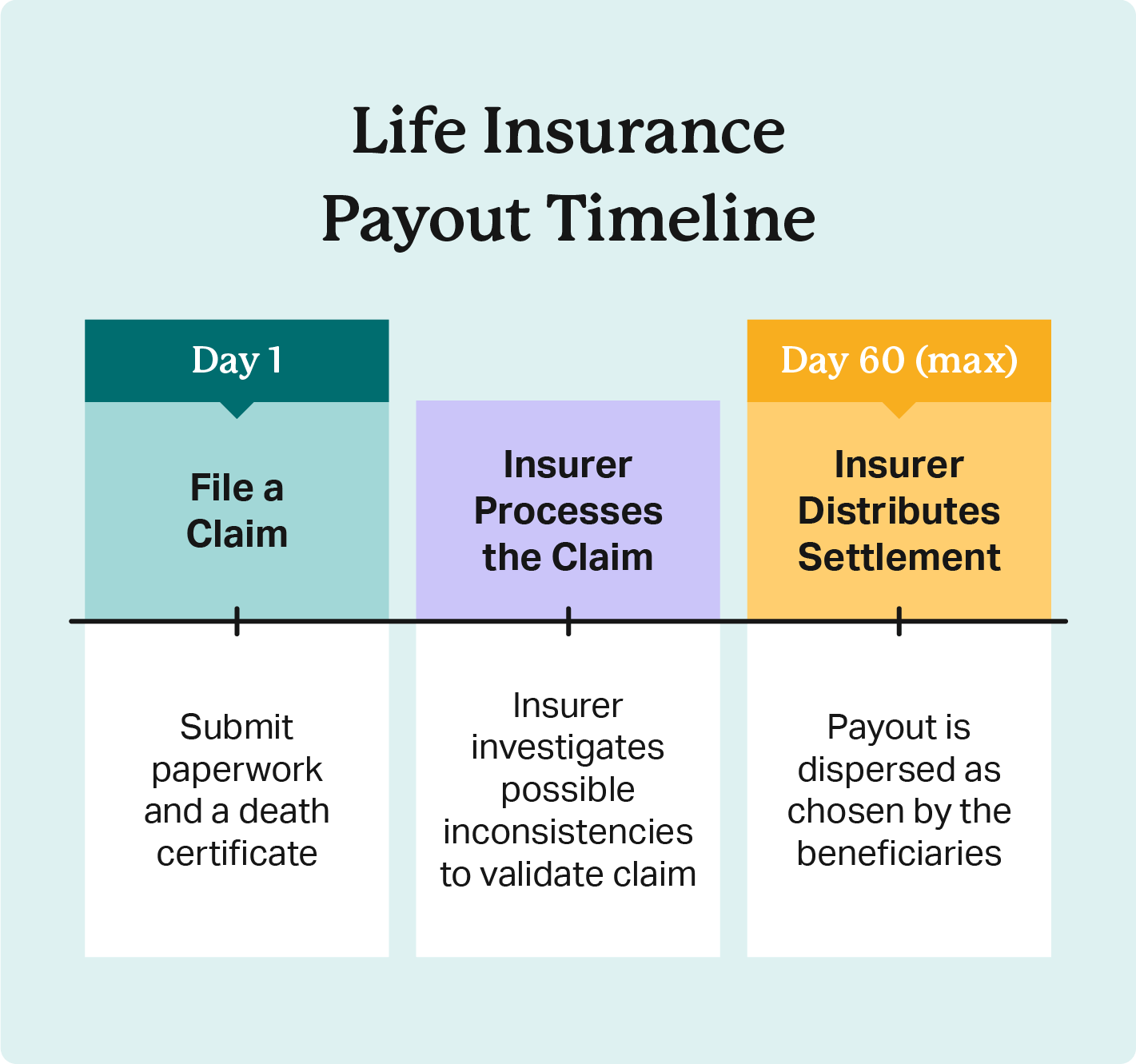

| Claim Process | Beneficiaries navigate complex paperwork after death | Policyholder accesses benefits with physician certification | Maintains control and agency |

The Industry Transformation: How Insurers Are Responding to Gen Z Demands

The Three Pillars of Modern Life Insurance Strategy

According to the Capgemini research, insurers who want to succeed with Gen Z must focus on three core transformations:

1. Innovate the Product:

- Launch flexible, modular solutions with living benefits at the core

- Simplify underwriting processes and reduce barriers to entry

- Gamify engagement through wellness programs and rewards

- Deliver tangible value across all life stages, not just at death

2. Enhance Distribution and Advisory:

- Equip agents with AI tools and customer insights for personalized guidance

- Create seamless omnichannel experiences combining digital convenience with human expertise

- Meet customers where they are: social media, financial planning apps, workplace platforms

- Provide education and transparency rather than just selling

3. Embrace Ecosystem Partnerships:

- Partner with wellness companies, fitness apps, and health platforms

- Integrate with financial services firms for comprehensive planning

- Embed insurance into everyday experiences through HR platforms and employee benefits

- Create value beyond insurance through health and wellness ecosystems

First Movers Gaining Competitive Advantage

Insurance companies that embrace these transformations early are capturing disproportionate market share among Gen Z:

Insurtech Disruptors: Companies like Ethos, Ladder, and Haven Life were built from the ground up for digital-native consumers, offering streamlined applications, transparent pricing, and modern benefits.

Traditional Insurers Modernizing: Companies like Northwestern Mutual, MassMutual, and Principal have invested heavily in digital platforms, living benefits products, and wellness integration to compete.

Wellness-Insurance Hybrids: Some companies are blurring the lines entirely, positioning themselves as wellness platforms that happen to include insurance rather than insurance companies with some wellness features.

The Competitive Threat From Adjacent Industries

Perhaps most concerning for traditional insurers: competition from unexpected sources. Financial wellness apps, employer benefits platforms, and even tech giants are entering the insurance space with Gen Z-friendly approaches:

- Apple Watch integration creating insurance-adjacent health monitoring

- Wearable technology companies partnering with insurers

- Financial planning apps offering insurance as part of comprehensive wealth management

- Employer benefits platforms embedding insurance into workplace offerings

These competitors understand digital engagement, wellness integration, and user experience in ways traditional insurers are still learning.

What This Means for Future Life Insurance Trends

The Great Wealth Transfer and Its Insurance Implications

Over the next 15-20 years, the largest intergenerational wealth transfer in history will occur as Baby Boomers pass assets to their children and grandchildren. Gen Z and millennials expect to inherit an average of $106,000 per person.

According to the Capgemini research, 40% of under-40 adults rank life insurance and annuities as the third most important destination for inherited funds, behind only stocks and cash savings.

This creates a massive opportunity—but only for insurers offering products that align with Gen Z values:

- Living benefits that provide security throughout life

- Flexible coverage that adapts to changing circumstances

- Wellness integration that supports healthy living

- Digital experiences that feel modern and accessible

- Transparent pricing and clear value propositions

Predictions for 2027 and Beyond

Based on current life insurance trends, here’s what we can expect:

Near-Term (2026-2027):

- Living benefits become standard on most policies, not optional riders

- Medical exams eliminated for majority of healthy applicants under 40

- AI-powered personalized pricing based on actual health data

- Instant approval becoming industry standard

- Wellness rewards programs expanding significantly

Medium-Term (2028-2030):

- Insurance fully embedded into wellness ecosystems and health apps

- Real-time premium adjustments based on verified health behaviors

- Blockchain-enabled portable health records improving underwriting

- Mental health coverage becoming as comprehensive as physical health

- Fertility and family planning support standard in modern policies

Long-Term (2031+):

- Continuous coverage model replacing annual renewals

- Predictive analytics preventing illnesses before they occur

- Integration with genetic testing for truly personalized coverage

- Universal living benefits across all policy types

- Insurance as a holistic life partnership rather than single product

The Policies That Will Win Gen Z

Successful modern life insurance products will share these characteristics:

Comprehensive Living Benefits: Not just death benefits, but robust coverage for critical illness, chronic conditions, terminal illness, plus wellness and preventive care support.

Radical Simplicity: Applications that take minutes, not hours. Coverage explanations anyone can understand. Transparent pricing with no hidden fees.

Digital Excellence: Mobile-first design, instant customer service, seamless policy management, and integration with other financial tools Gen Z already uses.

Value Throughout Life: Benefits that activate at multiple life stages, not just at death. Rewards for healthy behaviors. Support during career transitions, health challenges, and major life events.

Ethical Alignment: Companies that demonstrate genuine commitment to customer wellbeing, not just profit maximization. Transparent practices, fair pricing, and authentic support.

Practical Guidance: Should You Consider Living Benefits Insurance?

Who Should Prioritize Modern Life Insurance with Living Benefits

Living benefits insurance makes particular sense for:

Gig Economy Workers and Freelancers: If you lack employer-provided benefits, comprehensive life insurance with living benefits replaces the safety net traditional employment used to provide.

Young Adults With Debt: Student loans, credit card balances, and other obligations won’t disappear if you get sick. Living benefits ensure illness doesn’t also mean financial ruin.

First-Generation Wealth Builders: If you’re building financial security without family wealth to fall back on, protecting your progress against unexpected illness is crucial.

Anyone With Health Concerns in Their Family: If heart disease, cancer, or other serious conditions run in your family, living benefits provide crucial protection.

Entrepreneurs and Business Owners: Protecting your business, your income, and your personal finances requires more than traditional death benefits.

People Delaying Traditional Milestones: Even without a spouse or children currently, living benefits protect you during the years before you reach those milestones.

Questions to Ask When Evaluating Policies

About Living Benefits:

- Which conditions qualify for accelerated death benefits? (Critical, chronic, terminal illness)

- What percentage of the death benefit can be accessed while living? (25%-100% varies by policy)

- Are there waiting periods or restrictions on living benefits?

- What documentation is required to access benefits?

- Are living benefits included or do they cost extra?

About the Application Process:

- Can I apply entirely online?

- How long does approval typically take?

- Is a medical exam required for my age and coverage amount?

- Can I get a quote without providing contact information?

About Wellness and Additional Features:

- Does the policy include wellness rewards or preventive care incentives?

- Are there mental health support resources?

- Can I integrate with fitness trackers or health apps?

- What educational resources does the company provide?

About Flexibility and Cost:

- Can I adjust coverage as my income or needs change?

- What happens if I can’t pay premiums temporarily?

- How do premiums compare to traditional policies?

- Are there any hidden fees or charges?

Common Misconceptions Gen Z Should Ignore

Myth 1: “Life insurance is only for people with families.” Reality: Living benefits protect you first, not just your dependents. Even single, childless individuals benefit from critical illness coverage, chronic illness protection, and wellness support.

Myth 2: “I’m young and healthy, so I don’t need it yet.” Reality: Youth and health make coverage more affordable and easier to obtain. Waiting until you’re older or have health issues means paying significantly more or being denied coverage.

Myth 3: “Life insurance is too expensive.” Reality: Many Gen Zers drastically overestimate costs. A healthy 25-year-old can often get substantial coverage with living benefits for less than their monthly streaming subscriptions combined.

Myth 4: “The application process is too complicated and time-consuming.” Reality: Modern insurers offer applications that take 10-15 minutes online, with approval often within 24 hours and no medical exam required.

Myth 5: “I have employer-provided life insurance, so I’m covered.” Reality: Employer coverage is typically minimal (often just 1x your salary), disappears when you change jobs, and rarely includes comprehensive living benefits.

Conclusion: The Future of Life Insurance Is Living Benefits

The transformation happening in life insurance isn’t a minor trend—it’s a fundamental reimagining of what insurance should be. Gen Z isn’t rejecting life insurance; they’re rejecting an outdated model that no longer serves their reality.

Traditional death benefit-focused policies made sense for a different era: stable employment, predictable life milestones, employer-provided benefits, and lower healthcare costs. That world no longer exists for Gen Z.

Instead, today’s young adults face:

- Gig economy work without benefits

- Crushing debt from education and cost of living

- Delayed marriage and homeownership

- Unpredictable health challenges

- Economic uncertainty

- Wellness-focused values

- Digital-first expectations

Modern life insurance with living benefits addresses all of these realities. It provides:

- Protection you can use while alive through critical, chronic, and terminal illness coverage

- Wellness support that aligns with health-conscious values

- Flexibility that adapts to career changes and evolving needs

- Digital experiences that meet Gen Z’s expectations

- Comprehensive security for uncertain times

- Value throughout your entire life journey, not just at death

The life insurance trends of 2026 and beyond will be defined by how well insurers respond to these demands. Companies that innovate products, simplify experiences, and genuinely support their customers’ wellbeing will capture this generation’s loyalty for decades.

Those that cling to traditional models, opaque processes, and death-benefit-only thinking will find themselves increasingly irrelevant.

For Gen Z consumers, the message is clear: you don’t have to choose between protecting your present and securing your future. Modern life insurance with living benefits does both—and that’s exactly why it’s revolutionizing an industry that desperately needed change.

The future of life insurance isn’t about death. It’s about life—protecting it, enhancing it, and providing security throughout all of it.

Frequently Asked Questions (FAQs)

1. What does “living” life insurance coverage mean?

“Living” coverage refers to life insurance policies that provide benefits while you’re still alive—not just after death. These policies often include features like cash value access, living benefits for critical illness, disability income riders, mental health support, and wellness incentives. For Gen Z, the appeal lies in immediate, usable value rather than a distant payout.

2. Why is Gen Z rejecting traditional death-only life insurance?

Gen Z faces rising living costs, student debt, unstable job markets, and delayed milestones like homeownership and marriage. Traditional life insurance feels irrelevant when daily financial survival is the priority. Policies that only pay out after death don’t align with Gen Z’s short-term financial realities or mindset.

3. What types of “living benefits” matter most to Gen Z?

Gen Z gravitates toward policies offering critical illness coverage, income protection, emergency cash access, and digital-first experiences. Some modern policies also integrate financial planning tools, telemedicine, and wellness rewards—features that feel practical, flexible, and tech-friendly.

4. Is “living” coverage more expensive than traditional life insurance?

Not necessarily. Many living-benefit policies are modular, allowing Gen Z to customize coverage based on budget. While premiums may be slightly higher than basic term life insurance, the added value during one’s lifetime often outweighs the cost for younger consumers.

5. Are these policies still considered real life insurance?

Yes. Most living-coverage policies still include a death benefit. The difference is that they’re designed to support policyholders financially during illness, hardship, or major life disruptions—making them more versatile than traditional plans.

6. Will this trend continue beyond 2026?

All signs point to yes. As Gen Z becomes the dominant workforce generation, insurers are redesigning products around flexibility, transparency, and immediate value. Life insurance is evolving from a death-focused product into a holistic financial safety tool.