Introduction: Let me be brutally honest with you: most families are hemorrhaging money on term life insurance without even realizing it. In my years covering personal finance, I’ve watched countless households pay 50% to 70% more than necessary for the exact same coverage. The insurance industry isn’t exactly incentivized to advertise this fact, but the truth is that securing the best term life insurance in 2026 has less to do with luck and everything to do with strategy.

The landscape of term life insurance policies has shifted dramatically over the past few years. With increasing competition among carriers, advancing medical underwriting technology, and evolving consumer protections, savvy families are discovering they can lock in premium rates that would have seemed impossible just five years ago. Yet, simultaneously, millions of Americans continue overpaying simply because they don’t know the insider strategies that could save them thousands of dollars over the life of their policy.

This comprehensive guide reveals 11 powerful premium-saving strategies that the insurance industry would prefer you didn’t know about. Whether you’re purchasing your first policy or reevaluating existing coverage, these tactics will help you secure affordable term life insurance without sacrificing the protection your family deserves.

Understanding Term Life Insurance Rates in 2026: What’s Changed and Why It Matters

Before diving into money-saving strategies, let’s establish what we’re working with. Term life insurance rates in 2026 reflect a fascinating intersection of technological advancement, demographic shifts, and market competition that’s created unexpected opportunities for cost-conscious consumers.

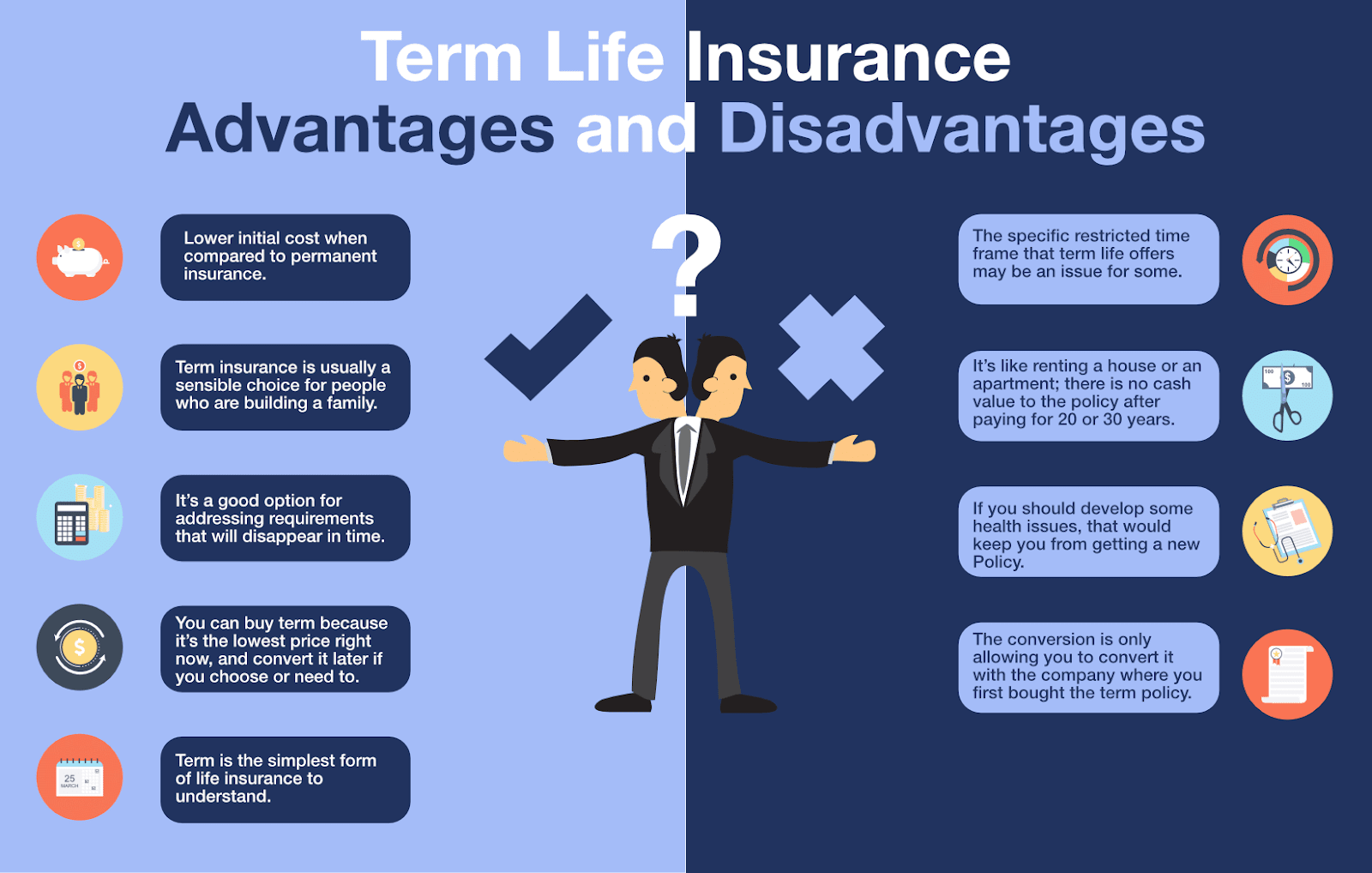

Term life insurance operates on a straightforward principle: you pay premiums for a specified period (the “term”), and if you pass away during that timeframe, your beneficiaries receive a death benefit. Unlike permanent life insurance, there’s no cash value component, which keeps costs substantially lower. For most families, this makes term policies the most practical and affordable term life insurance option.

The current rate environment has been influenced by several key factors. First, improved mortality tables show that people are living longer and healthier lives than previous generations, which has put downward pressure on premiums. Second, fierce competition among carriers—with over 800 life insurance companies operating in the United States—has created a buyer’s market where insurers are aggressively competing for your business.

Term Life Insurance Rates by Age in 2026: The Critical Timing Factor

Age remains the single most influential factor in determining your premium. The Insurance Information Institute consistently emphasizes that every year you wait translates into measurably higher costs. Here’s what term life insurance rates by age in 2026 typically look like for a healthy non-smoker purchasing a 20-year, $500,000 policy:

2026 Average Monthly Premium Estimates by Age

| Age Range | Male Monthly Premium | Female Monthly Premium | Annual Cost Increase vs. Previous Age Bracket |

|---|---|---|---|

| 25-29 | $18-$25 | $15-$21 | Baseline |

| 30-34 | $20-$28 | $17-$24 | 8-12% |

| 35-39 | $24-$35 | $21-$30 | 15-20% |

| 40-44 | $35-$50 | $30-$42 | 35-45% |

| 45-49 | $55-$78 | $45-$65 | 50-60% |

| 50-54 | $95-$135 | $75-$105 | 70-85% |

| 55-59 | $165-$230 | $125-$175 | 75-90% |

| 60-65 | $285-$400 | $210-$295 | 70-80% |

Note: Rates vary significantly based on health class, coverage amount, and carrier. These figures represent competitive market averages.

The exponential growth pattern here reveals a critical insight: delaying your purchase by even five years can effectively double your lifetime premium costs. For a 35-year-old versus a 40-year-old purchasing identical coverage, the difference over a 20-year term could exceed $7,200—money that could fund a child’s education or bolster retirement savings.

Strategy 1: Master the Art of Timing Your Best Term Life Insurance Purchase

Timing isn’t just important when securing the best term life insurance policies in 2026—it’s everything. The insurance industry operates on precise actuarial tables that adjust premiums based on your age at the time of application, and understanding these age brackets can save you thousands.

Insurance companies typically recalculate rates in six-month or annual increments based on your age. Here’s where it gets interesting: most carriers use your “insurance age” rather than your actual birthday. Your insurance age is generally your age on your nearest birthday, which means if you’re 35 years and 7 months old, you’re considered 36 for rating purposes.

The Strategic Timing Advantage:

If you’re approaching a birthday that will push you into a higher age bracket, accelerating your application by even a few weeks can lock in lower rates for the entire term. Conversely, if you just had a birthday, you have nearly 12 months before age becomes a factor again.

Consider Sarah’s situation: At 39 years and 11 months, she delayed her application thinking she needed to “get more organized first.” By the time she applied at 40 years and 1 month, her quotes had increased by $420 annually for the same coverage—a total difference of $8,400 over her 20-year term. Had she prioritized the application before her birthday, she would have locked in the lower rate indefinitely.

Action Steps for Optimal Timing:

- Check your insurance age calculation with prospective carriers during the quote process

- Begin shopping 60-90 days before your birthday if you’re approaching a rate-increase threshold

- Don’t wait for “perfect health”—minor improvements in health metrics rarely offset the cost of aging into the next bracket

- Consider term length strategically—your current age impacts which term lengths offer the best value

- Lock rates with applications, not just quotes—submitted applications typically freeze your age for underwriting purposes

The psychological barrier many people face is the urgency factor. Unlike buying a car or planning a vacation, life insurance feels like something you can always do “next month.” This procrastination bias costs American families an estimated $3.2 billion annually in unnecessarily higher premiums. The carriers understand human psychology, and they profit handsomely from our tendency to delay.

Strategy 2: Leverage the Hidden Power of Health Classifications for Affordable Term Life Insurance

Most people assume they’re “average” health-wise and will therefore receive standard rates. This assumption costs them dearly. The truth about affordable term life insurance is that the industry uses nuanced health classifications that can slash your premiums by 30% to 60%—but only if you understand how to qualify.

Understanding the Health Class Hierarchy

Insurance carriers typically use four to six health classifications, though exact naming conventions vary:

Preferred Plus/Elite: The golden tier, typically reserved for the healthiest 5-10% of applicants. Requires excellent health metrics, no tobacco use, favorable family history, and often a healthy BMI (body mass index) ratio.

Preferred: Still excellent rates, capturing the top 25-30% of applicants. Slightly more flexible on metrics but still requires strong overall health profile.

Standard Plus: Above-average health, representing about 30% of applicants. Minor health considerations or family history issues may place you here.

Standard: The baseline classification, where about 25-30% of applicants land. Represents average health with some considerations.

Substandard/Table Ratings: Reserved for significant health issues, these classifications add percentage increases to standard rates.

Here’s what many agents won’t proactively tell you: the difference between Standard and Preferred Plus on a $500,000, 20-year term for a 40-year-old could be $180 versus $290 monthly—a staggering $26,400 over the life of the policy.

Optimizing Your Health Profile Before Applying

The best term life insurance policies in 2026 reward preparation. Unlike health insurance under the Affordable Care Act (which prohibits medical underwriting for most plans), life insurers still evaluate your individual risk meticulously. Smart applicants optimize their health metrics before the medical exam:

90-Day Pre-Application Optimization Protocol:

- Blood Pressure Management: Even borderline readings can knock you down a health class. If you’re between 120/80 and 130/85, consider sodium reduction, stress management, and potentially discussing medication with your physician. Many applicants don’t realize that well-controlled hypertension with medication can still qualify for preferred rates.

- Cholesterol Panel Preparation: Your total cholesterol, LDL, HDL, and triglycerides all factor into classification. The 8 weeks before your exam is crucial—increase omega-3 intake, reduce saturated fats, and consider supplementation after consulting with a healthcare provider.

- Glucose and A1C Levels: Prediabetic readings (fasting glucose 100-125 mg/dL or A1C 5.7-6.4%) can drop you multiple health classes. Implementing moderate carbohydrate restriction and increasing physical activity can show measurable improvements in 60-90 days.

- BMI Optimization: While you can’t dramatically change body composition overnight, even 5-10 pounds can move you from one BMI category to another. Insurance companies use strict height-weight tables, so knowing your target weight for preferred classifications is essential.

- Liver Enzymes (ALT/AST): Elevated readings often result from alcohol consumption, certain medications, or fatty liver disease. A 30-day alcohol abstention before your exam can normalize these values for many applicants.

Michael’s experience illustrates this perfectly. As a 44-year-old seeking $750,000 in coverage, his initial informal assessment suggested Standard rates at $124 monthly. Rather than applying immediately, he spent 10 weeks working with his doctor to optimize his health metrics—losing 12 pounds, reducing his LDL cholesterol through dietary changes, and managing his borderline blood pressure through stress reduction techniques.

When he applied, his improved metrics qualified him for Preferred Plus classification at $78 monthly—a savings of $46 monthly or $11,040 over his 20-year term. The investment of 10 weeks of focused health improvement returned over $11,000 in savings. That’s a return on investment you won’t find in any stock market.

The Medication Consideration:

One counterintuitive insight: being on medication for a well-controlled condition is often better than having borderline numbers without treatment. Carriers view medication compliance as responsible health management. A person with high blood pressure taking prescribed medication and showing controlled readings will typically receive better classification than someone with borderline readings who refuses treatment.

Strategy 3: Exploit Multi-Policy Bundling for the Cheapest Term Life Insurance for Families in 2026

When searching for the cheapest term life insurance for families in 2026, most people make the critical mistake of viewing life insurance in isolation. The carriers who offer the most aggressive rates understand cross-selling opportunities, and they’re willing to offer substantial discounts when you bundle multiple policies or products.

The bundling advantage operates on several levels, and understanding each can compound your savings exponentially.

Spousal Bundling Discounts

Many top carriers offer 5% to 15% discounts when both spouses purchase policies simultaneously from the same company. This isn’t merely a courtesy discount—it represents genuine cost savings for the insurer through consolidated underwriting, single medical examination scheduling, and reduced administrative overhead.

For a couple both purchasing $500,000 policies with a 10% joint discount, this translates to roughly $1,800 to $3,000 in savings over a 20-year term. But the strategy goes deeper than just asking for a discount.

Advanced Spousal Bundling Tactics:

- Coordinate health classifications: If one spouse qualifies for superior health ratings, some carriers extend preferential consideration to the other spouse, particularly when health metrics are close to classification thresholds.

- Strategic coverage amounts: Rather than mirroring coverage amounts, optimize based on actual need (typically higher for the primary earner) while still qualifying for joint policy benefits.

- Synchronize term lengths: Matching policy term lengths simplifies future renewals and often qualifies for additional administrative discounts.

Cross-Product Bundling

The real hidden opportunity lies in cross-product bundling with the same carrier. Many life insurance companies also offer auto, home, disability, and umbrella liability coverage. While you might not think of these products as related, carriers definitely do.

According to consumer advocacy research, policyholders who maintain three or more products with the same carrier can access preferential underwriting that effectively moves them up one health classification, plus explicit premium reductions of 8% to 20%.

Real-World Cross-Product Bundling Example:

Jennifer and David were quoted $2,856 annually for a combined $1.5 million in term coverage from a mid-tier carrier. When they discovered the same company offered competitive auto and umbrella liability policies, they requested a comprehensive quote across all products.

The result? Their life insurance premium dropped to $2,285 annually (a 20% reduction), while their auto insurance actually came in $180 less per year than their previous carrier, and they added a $2 million umbrella policy for just $420 annually. The total household insurance cost decreased by $751 annually while substantially increasing their overall protection—a masterclass in strategic bundling.

The Employer Policy Trap

Here’s a critical warning about what might seem like the ultimate “bundle”—relying on employer-provided group term life insurance. While employer policies offer convenience and guaranteed issue (no medical underwriting), they typically cost 30% to 200% more than individual policies when you calculate the true cost.

Employers often subsidize a base amount (often 1-2x annual salary), but supplemental coverage purchased through your employer uses group rates that don’t consider your individual health. A healthy 35-year-old purchasing $500,000 through an employer group plan might pay $45-$65 monthly, while an individual policy based on their health profile would cost $22-$28 monthly.

Additionally, employer coverage is rarely portable—when you change jobs or retire, you lose coverage or face exorbitant conversion costs. The best term life insurance strategy is owning an individual policy you control, treating any employer-provided coverage as a supplement rather than your primary protection.

Strategy 4: Understand the Annual vs. Monthly Payment Arbitrage for Best Term Life Insurance Value

A deceptively simple strategy that most families overlook when securing the best term life insurance policies in 2026 is payment frequency optimization. The way you pay your premiums can impact your total cost by 4% to 12% annually—potentially thousands of dollars over your policy term.

Insurance carriers face real costs processing monthly payments: bank transaction fees, administrative overhead, collection management, and most significantly, the opportunity cost of delayed premium collection. To offset these costs and encourage annual payments, most insurers offer discounts when you pay your full annual premium upfront.

The Real Math Behind Payment Mode Savings

Let’s examine the actual numbers. For a $1,200 annual premium paid monthly, the total cost might be $1,272 to $1,320 when you include monthly payment fees and the interest factor built into installment plans. That’s an extra $72 to $120 annually—$1,440 to $2,400 over a 20-year term—for the convenience of monthly payments.

Annual Payment Advantages:

- Direct premium discounts: 4-8% reduction off the annual base premium

- No payment processing fees: Savings of $2-$5 per monthly transaction

- Avoid interest charges: Many monthly plans include implicit interest of 6-10% APR

- Reduce lapse risk: Single annual payment eliminates 11 opportunities for payment failure

- Simplify cash flow management: One annual transaction instead of 12

When Monthly Payments Make Strategic Sense:

Despite these advantages, monthly payments aren’t always the wrong choice. For families with variable income, tight monthly budgets, or those building emergency funds, the cash flow management benefit of monthly payments can outweigh the premium cost.

The key is making an informed decision rather than defaulting to monthly payments out of habit. If you’re paying an extra $100 annually for monthly payment convenience but have $5,000 sitting in a checking account earning 0.5% interest, you’re making an irrational financial decision. Conversely, if paying annually would drain your emergency fund, the security of maintaining liquidity might justify the premium surcharge.

The Hybrid Approach: Semi-Annual Payments

Many carriers offer a middle ground: semi-annual payments. This option typically captures 60-75% of the annual payment discount while requiring only two payments per year. For policies with $1,200 annual premiums, semi-annual payments might cost $1,236 total versus $1,200 annual or $1,296 monthly—splitting the difference while maintaining reasonable cash flow management.

Advanced Payment Strategy:

Open a dedicated savings account and automate monthly transfers equal to your monthly premium amount. When your annual payment comes due, you’ve automatically accumulated the funds while earning interest on the balance throughout the year. This discipline provides monthly budget predictability while capturing the full annual payment discount.

Robert implemented this strategy with his $2,400 annual premium, setting aside $200 monthly into a high-yield savings account earning 4.5% APY. Over the year, he earned approximately $50 in interest while preparing for his annual payment—effectively reducing his net premium cost by an additional 2% beyond the annual payment discount he was already receiving.

Strategy 5: Navigate Riders and Add-Ons Without Destroying Your Affordable Term Life Insurance Rates

The term life insurance policies marketplace in 2026 has exploded with optional riders and add-ons, many of which sound compelling but dramatically inflate your premiums. Understanding which riders provide genuine value versus which represent pure profit centers for carriers is essential to maintaining affordable term life insurance.

The Rider Value Assessment Framework

Every rider should pass a simple cost-benefit analysis: Does the additional premium cost justify the incremental protection, or would purchasing separate coverage (or self-insuring) prove more economical?

Riders Worth Considering:

Convertibility Rider (Often Included Free): This allows you to convert your term policy to permanent coverage without new medical underwriting. While most people won’t use this feature, having it costs nothing with most quality carriers and provides valuable optionality if health changes prevent future insurability.

Accelerated Death Benefit (Usually Included): Permits accessing a portion of your death benefit if diagnosed with a terminal illness. Most modern policies include this at no charge—verify this before purchasing separate critical illness coverage that duplicates this benefit.

Waiver of Premium for Disability: If you become disabled and can’t work, this rider waives your life insurance premiums while maintaining your coverage. For a 40-year-old with a $500,000 policy, this might cost $8-$15 monthly. Whether this makes sense depends on your existing disability insurance coverage and financial reserves.

Child Term Rider: Adds modest life insurance on children (typically $10,000-$25,000) for $5-$8 monthly per family. While child death is statistically unlikely, the modest cost and guaranteed future insurability conversion option can provide value for some families.

Riders to Approach Skeptically:

Accidental Death Benefit (Double Indemnity): Pays an additional benefit if death results from an accident. This sounds attractive but is almost always poor value—your family’s financial need doesn’t change based on how you die. If you need $750,000 in coverage, buy $750,000, not $500,000 with an accidental death rider. The premium savings from avoiding this rider often exceeds 10-15%.

Return of Premium (ROP): This rider returns all paid premiums if you outlive your term—at a cost of 30-70% higher premiums. The math rarely works out. A $30 monthly policy might become $48 monthly with ROP. Over 20 years, you pay an extra $4,320 to get back $7,200—but investing that $18 monthly difference at 7% returns would grow to $9,373, almost $2,000 more than the ROP benefit. This rider primarily benefits people who lack investment discipline.

Living Benefits/Critical Illness Riders: These allow accessing your death benefit if diagnosed with specified critical illnesses. Costs vary widely (8-25% premium increase), and coverage is typically riddled with exclusions and limitations. Standalone critical illness or disability insurance usually provides superior value if you need this protection.

The Riders Decision Matrix

| Rider Type | Average Cost Impact | Value Proposition | Better Alternative? |

|---|---|---|---|

| Convertibility | 0% (included) | High – provides future insurability option | None – always include if available |

| Accelerated Death Benefit | 0-2% | High – terminal illness access | None – typically included free |

| Waiver of Premium | 3-5% | Moderate – depends on disability coverage | Comprehensive disability insurance |

| Child Term | 2-4% | Moderate – depends on family situation | Separate child policy or savings |

| Accidental Death | 10-15% | Low – arbitrary benefit trigger | Purchase adequate base coverage |

| Return of Premium | 30-70% | Very Low – poor investment return | Invest premium difference separately |

| Critical Illness | 15-30% | Low – better standalone options available | Standalone critical illness or disability |

The “No Riders” Strategy:

For most families seeking the cheapest term life insurance for families in 2026, the optimal approach is purchasing adequate base coverage without adding riders (except those included free). This maximizes death benefit per premium dollar spent while avoiding the complexity and exclusions that plague many riders.

Amanda and Tom discovered this when comparing quotes. One carrier offered them $1 million coverage at $95 monthly with no riders. Another quoted $1.2 million at $102 monthly with accidental death benefit, return of premium, and critical illness riders. While the second quote appeared to offer “more,” analyzing the actual protection revealed the first option provided 25% more guaranteed death benefit at lower cost. They selected the straightforward $1 million policy and invested the savings—a decision that provided both superior protection and wealth building.

Strategy 6: Deploy the Medical Exam Gaming Strategy (Ethically and Legally)

Let’s address something that makes insurance companies uncomfortable: the medical examination for your best term life insurance policy isn’t a neutral scientific measurement—it’s a high-stakes performance that can be optimized. I’m not suggesting deception or fraud (which is illegal and will void your coverage), but rather understanding that your medical exam results represent a snapshot in time that can be influenced by numerous controllable variables.

The 48-Hour Pre-Exam Protocol

Your medical exam typically includes blood pressure readings, blood work (cholesterol panel, glucose, liver enzymes, kidney function), urinalysis, height and weight measurements, and sometimes an EKG. Each of these metrics fluctuates based on your recent behaviors, and understanding these fluctuations is crucial.

Blood Pressure Optimization:

Blood pressure readings are notoriously variable, influenced by stress, caffeine, sodium intake, hydration status, and even time of day. Insurance companies know this, which is why many allow multiple readings if the first is elevated.

Strategic considerations for the 48 hours before your exam include avoiding caffeine entirely (even morning coffee can elevate readings for 3-4 hours), reducing sodium intake to under 1,500mg daily, staying well-hydrated (dehydration can raise blood pressure), getting 7-8 hours of quality sleep the night before, and avoiding strenuous exercise 24 hours prior to your exam (which can temporarily elevate readings).

During the exam itself, request to sit quietly for 5-10 minutes before measurement, ensure proper cuff sizing and arm positioning, and utilize slow, deep breathing during measurement. If the first reading is high, politely request a second measurement after additional rest—many examiners will accommodate this.

Blood Panel Preparation:

Your blood work requires fasting (typically 8-12 hours) and is influenced by your diet in the 24-72 hours preceding the draw.

For cholesterol optimization, avoid high-fat meals for 48 hours before the exam (even “healthy” fats from nuts, avocados, and fish can temporarily elevate readings), increase fiber intake from vegetables and whole grains in the days before, and consider the timing of any fish oil supplementation (which can affect triglyceride readings).

For glucose and A1C optimization, follow prescribed fasting guidelines precisely, avoid simple carbohydrates and sugars for 48 hours prior, and be aware that stress and poor sleep can elevate glucose readings independent of diet.

Liver enzyme readings (ALT, AST, GGT) can be elevated by alcohol consumption, certain medications, supplements (particularly high-dose vitamin A or certain herbal products), and intense exercise. A 7-10 day abstention from alcohol before your exam can normalize readings for most people.

The Hydration Strategy:

Proper hydration affects multiple health markers. Dehydration can elevate blood pressure, increase protein concentration in urine, affect kidney function markers, and even impact blood glucose readings. The 24 hours before your exam, focus on consuming water consistently (aim for half your body weight in ounces as a general guideline).

However, avoid the common mistake of dramatically overhydrating immediately before your exam—this can dilute your urine to the point where the specific gravity is abnormal, potentially triggering additional testing or questions about whether you were attempting to mask substance use.

The Timing and Scheduling Advantage

Request your medical exam during your optimal performance window. For most people, mid-morning (9-11 AM) provides the best combination of factors: you’ve had time to wake up fully and normalize from sleep, you’re not yet stressed from the day’s activities, fasting from the previous evening is easily manageable, and cortisol levels (which affect multiple health markers) have normalized from their morning peak.

Avoid scheduling exams on Mondays (when you might still be recovering from weekend indulgences) or Fridays (when you might be stressed or fatigued from the week). Mid-week scheduling often produces optimal results.

The Portable Medical Exam Advantage:

Many insurers offer portable medical exams at your home or office. While convenient, these can introduce additional stress (the novelty of having a medical professional in your home, rushing to prepare, etc.). If you’re someone who experiences “white coat syndrome,” requesting an exam at a familiar location where you can control the environment might produce better results.

Strategy 7: Master the Art of Company Comparison for Best Term Life Insurance Policies in 2026

Perhaps the most powerful premium-saving strategy when seeking the best term life insurance policies in 2026 is understanding that pricing variation among carriers can exceed 50% for identical coverage—yet most consumers only compare two or three companies before purchasing.

The life insurance industry operates on specialized underwriting philosophies, with each carrier developing niches based on specific risk factors, health conditions, occupations, and hobbies. What one company views as high-risk might be standard for another, creating dramatic rate disparities for certain applicant profiles.

The Company Specialization Landscape

Health Condition Specializations:

Some carriers have developed expertise in specific health conditions and offer preferential underwriting accordingly. For instance, applicants with well-controlled diabetes might find certain carriers offering rates 20-40% better than competitors. Similarly, some companies specialize in applicants with cardiovascular history, thyroid conditions, or mental health histories.

This specialization creates an opportunity: by working with an independent broker who understands these niches or by researching carrier philosophies yourself, you can target companies most likely to offer competitive rates for your specific health profile.

Lifestyle and Occupation Niches:

Certain carriers actively court specific occupational or lifestyle groups. Some companies offer standard rates for pilots (where others impose aviation exclusions or surcharges), competitive rates for law enforcement or firefighters, or favorable underwriting for foreign travel or adventure sports enthusiasts.

Jacob, a 38-year-old pilot and avid scuba diver, received quotes ranging from $78 to $186 monthly for identical $750,000 coverage. The variation wasn’t due to different health assessments—it reflected each carrier’s appetite for his occupation and hobby risk profile. By identifying the two carriers known for favorable pilot underwriting, he secured coverage at $82 monthly versus the $186 from a carrier that viewed aviation as high-risk.

The Independent Broker Advantage

While buying direct from carriers might seem cost-effective, working with an independent broker typically produces better results when securing affordable term life insurance. Quality independent brokers maintain contracts with 20-40 carriers and understand their underwriting nuances.

Critically, broker commissions are typically identical across carriers and are built into the premium structure—meaning you pay the same amount whether you work with a broker or buy direct, but with a broker you access their market knowledge and advocacy during underwriting.

How to Identify Quality Independent Brokers:

Look for brokers who represent at least 15+ carriers (more options mean better likelihood of finding your optimal match), have professional designations like CLU (Chartered Life Underwriter) or CFP (Certified Financial Planner), provide written comparison illustrations from multiple carriers, explain the underwriting strengths of different companies for your profile, and don’t pressure you toward one specific carrier.

Red flags include brokers who show you only one or two options, who can’t explain why they’re recommending a specific carrier, who pressure you to purchase immediately, or who disparage all other options as inferior without specific reasoning.

The DIY Comparison Approach:

For those who prefer researching independently, online comparison tools have improved substantially. However, be aware that many comparison sites are actually lead generation tools for specific carriers or brokers—they may not show the full market.

A comprehensive DIY comparison approach involves using at least three independent comparison tools, requesting quotes directly from highly-rated carriers identified in your research, and verifying that you’re comparing identical coverage (same term length, coverage amount, and rider options).

The Rate Variation Reality:

To illustrate the importance of comparison shopping, consider this real-world data from 2026 quotes for a healthy 42-year-old male seeking $500,000, 20-year term coverage:

Sample Rate Comparison Across Eight Major Carriers

| Insurance Carrier | Monthly Premium | Annual Cost | 20-Year Total Cost | Variance from Lowest |

|---|---|---|---|---|

| Carrier A | $48 | $576 | $11,520 | Baseline |

| Carrier B | $52 | $624 | $12,480 | +$960 |

| Carrier C | $54 | $648 | $12,960 | +$1,440 |

| Carrier D | $58 | $696 | $13,920 | +$2,400 |

| Carrier E | $62 | $744 | $14,880 | +$3,360 |

| Carrier F | $67 | $804 | $16,080 | +$4,560 |

| Carrier G | $71 | $852 | $17,040 | +$5,520 |

| Carrier H | $73 | $876 | $17,520 | +$6,000 |

Note: Same applicant profile, identical coverage specifications. Rates obtained through independent broker on same date.

The difference between the highest and lowest quote exceeds $6,000 over the policy term—for identical coverage protecting the same person. This 52% price variation for the same product would be unconscionable in most industries, yet it’s standard in life insurance because most consumers don’t compare thoroughly.

The Financial Strength Consideration

While price matters, it shouldn’t be your only consideration. Your insurer needs to exist and remain financially stable for potentially 20-30 years. Rating agencies like A.M. Best, Moody’s, Standard & Poor’s, and Fitch evaluate insurance company financial strength.

Generally, stick with carriers rated A- or higher by A.M. Best (or equivalent ratings from other agencies). The premium savings from a B+ rated carrier versus an A+ carrier might be 5-8%, but the financial stability risk isn’t worth the modest savings. Your beneficiaries need confidence that the company will be able to pay claims decades from now.

Strategy 8: Understand the Ladder Strategy for Maximum Term Life Insurance Value

One of the most sophisticated yet underutilized approaches to securing affordable term life insurance is the ladder strategy—purchasing multiple policies with staggered term lengths and decreasing coverage amounts that align with your evolving financial needs.

Most families default to purchasing a single large policy with a 20 or 30-year term. While simple, this approach often results in overpaying for coverage you don’t need in later years or underinsuring critical earlier years when your financial obligations are highest.

The Laddering Concept Explained

The ladder strategy recognizes that your life insurance needs decrease over time as you accumulate assets, pay down debt, and approach retirement. A 35-year-old couple with a new mortgage, young children, and minimal savings might need $1.5 million in coverage. That same couple at age 55 likely needs only $400,000, assuming they’ve paid down debt, accumulated retirement savings, and have children nearing independence.

Rather than purchasing $1.5 million of 30-year coverage (and paying for coverage you don’t need in years 20-30), the ladder approach might structure coverage as $500,000 for 30 years, $500,000 for 20 years, and $500,000 for 10 years—providing $1.5 million total coverage initially, stepping down to $1 million after 10 years and $500,000 after 20 years.

The Mathematical Advantage

Let’s compare the costs for a healthy 35-year-old male:

Traditional Single Policy Approach:

- $1.5 million, 30-year term: $145 monthly ($52,200 total over 30 years)

Laddered Approach:

- $500,000, 30-year term: $48 monthly

- $500,000, 20-year term: $32 monthly

- $500,000, 10-year term: $18 monthly

- Combined: $98 monthly ($35,280 total over 30 years)

The ladder strategy provides identical coverage during the critical high-need years (ages 35-45) while saving $16,920 over 30 years—a 32% reduction in total premium costs. Additionally, the shorter-term policies can often be purchased at better health classifications since you’re younger when applying, and the smaller policy amounts may require less stringent underwriting.

Optimizing Your Ladder Structure

The optimal ladder design depends on your specific financial trajectory, but common structures include:

Young Family Ladder (ages 30-35):

- 30-year term covering mortgage balance

- 20-year term covering children’s education costs

- 10-year term covering income replacement during highest earning years

Mid-Career Ladder (ages 40-45):

- 25-year term for remaining mortgage and final education years

- 15-year term for income replacement until children are independent

- 10-year term for transition into retirement years

Pre-Retirement Ladder (ages 50-55):

- 15-year term covering final working years

- 10-year term for early retirement gap coverage

Advanced Laddering Tactics:

Purchase all ladder policies simultaneously to lock in current age ratings and complete medical underwriting once. This also allows you to potentially leverage spousal bundling discounts across multiple policies.

Consider slight overlap in term end dates rather than precise alignment—this provides flexibility if you need to convert one policy to permanent insurance or extend coverage without new underwriting.

Some carriers offer multi-policy discounts when you purchase several policies simultaneously, effectively making the ladder strategy even more economical.

When Laddering Doesn’t Make Sense

The ladder strategy works best for families with predictable, decreasing insurance needs over time. It’s less optimal if you anticipate needing consistent coverage throughout the term (perhaps due to special needs dependents, estate planning considerations, or business obligations), if you have unpredictable health that might make future insurability uncertain, or if your financial obligations might increase rather than decrease (caring for aging parents, etc.).

Additionally, the administrative complexity of managing three policies versus one can be a consideration—though modern automatic payment systems make this largely negligible.

Strategy 9: Exploit the Application Timing Strategy to Lock in Low Term Life Insurance Premiums

A lesser-known but powerful strategy when seeking to lock in low term life insurance premiums involves understanding the optimal sequence and timing of your policy applications, particularly if you’re purchasing coverage for multiple family members or stacking policies in a ladder strategy.

The Application Order Optimization

Insurance companies share information through the Medical Information Bureau (MIB), a clearinghouse that tracks your life insurance applications and medical exam results. While this prevents fraud and duplicate coverage issues, it also creates strategic considerations for how you sequence multiple applications.

The Simultaneous Application Advantage:

When both spouses need coverage, applying simultaneously—ideally with the same carrier—provides several benefits. You lock in current age ratings for both parties, complete the medical examination process efficiently (often a single visit from a paramedical examiner), leverage any spousal discount programs, and avoid the situation where one spouse’s exam results might influence the other’s underwriting.

Consider the Martinez family scenario: Elena applied for coverage first, and her medical exam revealed borderline glucose readings (101 mg/dL, just above the normal threshold). While she still received coverage, the MIB record created additional scrutiny when her husband Carlos applied three months later to a different carrier. Despite Carlos having perfect glucose levels, the underwriter saw Elena’s reading in the MIB report and questioned whether there might be shared lifestyle factors affecting both spouses.

This additional scrutiny delayed Carlos’s approval and nearly resulted in a health classification downgrade. Had they applied simultaneously, each would have been evaluated independently on their own merits, and Carlos’s application wouldn’t have been influenced by Elena’s borderline reading.

The Health Trajectory Timing

If you’re managing a health condition, timing your application relative to your health trajectory can dramatically impact rates. Generally, you want to apply when you can demonstrate the longest period of stable, well-controlled health metrics.

Examples of Strategic Health Timing:

If you’ve recently lost significant weight, wait until you’ve maintained your new weight for at least six months before applying—demonstrating sustainability rather than temporary loss.

For those who’ve quit smoking, most carriers offer tobacco-free rates after 12 months of cessation, though some require 24 months. Knowing each carrier’s specific requirements allows you to time applications optimally.

If you’ve had a recent health event (surgery, hospitalization, concerning test results), waiting until you have 6-12 months of normal follow-up results can mean the difference between decline, table ratings, or standard approval.

Conversely, if you have a progressive condition that might worsen, applying earlier while your health is relatively stable makes sense—future deterioration won’t affect an in-force policy.

The Reapplication Strategy

Here’s a tactic few people consider: if you purchased a policy several years ago when your health was suboptimal or you were overweight, but you’ve since improved significantly, you may qualify for better rates with a new application. The existing policy provides protection while you apply elsewhere, and if approved at better rates, you can cancel the original policy.

Mark’s situation illustrates this perfectly. At age 42, following a divorce and period of poor health habits, he purchased a $500,000 policy at Standard rates for $87 monthly. Over the next three years, he lost 40 pounds, lowered his cholesterol significantly, and brought his blood pressure under control through lifestyle changes.

At age 45, he applied for a new policy and qualified for Preferred Plus classification—$59 monthly for the same coverage. Despite being three years older, his improved health and classification resulted in a 32% premium reduction. He was saving $336 annually, and over the remaining 17 years of his term, this strategy would save him $5,712.

Reapplication Considerations:

Never cancel your existing policy until the new policy is issued and in force—you need continuous coverage protection. Review your existing policy’s conversion options before canceling (sometimes older policies have more favorable conversion terms). Calculate the break-even point: the premium savings must justify the effort of reapplying and potentially paying for a new medical exam (though many carriers provide this free).

Be aware that age increases may partially offset health improvements, so run the numbers carefully. Some carriers offer internal policy reconsideration if your health has improved dramatically, which might be simpler than reapplying elsewhere.

Strategy 10: Understand the Underwriting Process to Accelerate Approval and Secure Better Term Life Insurance Rates

The term life insurance rates you ultimately receive depend not just on your health but on how effectively you navigate the underwriting process. Understanding what underwriters evaluate and proactively providing context can mean the difference between standard and preferred classifications.

The Underwriting Investigation

Modern life insurance underwriting involves several data sources beyond your medical exam: your application details and medical history questionnaire, prescription drug database checks (showing what medications you’ve been prescribed), motor vehicle records (evaluating driving history), MIB reports (prior insurance applications and outcomes), and sometimes attending physician statements (APS) requesting records from your doctors.

Each of these sources can reveal information requiring explanation or context, and how you handle these questions significantly impacts your outcome.

The Medical History Disclosure Strategy

One of the most common questions I receive is whether to disclose minor health issues or past treatments on the application. The answer is unequivocally yes—always disclose fully and honestly. Insurance fraud is a serious legal issue, and more practically, carriers will discover undisclosed conditions through their investigation process. An undisclosed condition found during underwriting results in immediate decline and an MIB record that will haunt future applications.

However, disclosure doesn’t mean passive acceptance of whatever classification the insurer assigns. Strategic disclosure involves providing context that helps underwriters understand your situation:

Effective Medical History Contextualization:

For past conditions that have fully resolved, include specific dates of diagnosis, treatment, and resolution, along with current status confirmation from your physician if available.

For ongoing conditions being managed, emphasize stability, compliance with treatment, and normal follow-up test results.

For family history concerns, distinguish between immediate family (parents, siblings) and extended family—underwriters weight these differently.

For medications, explain the indication—some medications are prescribed for multiple conditions, some serious and some benign. Proactive clarification can prevent misunderstandings.

Example of Strategic Disclosure:

Rather than simply checking “yes” for “Have you been treated for mental health conditions?” and listing “depression,” a more strategic disclosure might state: “Brief reactive depression following father’s death in 2020, treated with Sertraline 50mg for 18 months, discontinued June 2021 with physician approval, no recurrence, no current symptoms or treatment. Complete records available from Dr. Sarah Johnson if needed.”

This disclosure is honest and complete but provides context that helps the underwriter understand this was a situational response to a specific stressor rather than chronic depression—potentially preventing an automatic classification downgrade.

The Prescription Drug Database Explanation

Prescription databases reveal every medication you’ve been prescribed, even if you never filled it or only used it briefly. This often creates confusion during underwriting when the database shows medications the applicant doesn’t recall or that were prescribed but not actually taken.

Proactive strategy: Before applying, request your prescription history from your pharmacy or through your health insurance. Review it for accuracy and be prepared to explain any medications listed, particularly those that might raise underwriting concerns. If a medication was prescribed but never filled or used, stating this upfront prevents the underwriter from assuming you’re currently taking it.

The Attending Physician Statement Management

For complex medical histories, insurers often request Attending Physician Statements (APS)—medical records from your doctors. This process can delay approval by weeks and sometimes reveals information that complicates underwriting.

APS Acceleration Tactics:

When you sign the authorization allowing the insurer to request records, also contact your physician’s office directly, explain that you’ve applied for life insurance and an APS request is coming, and ask them to prioritize the response. Many offices process insurance requests slowly unless patients specifically request expediting.

If you know specific health issues will require records, proactively gather recent test results, treatment summaries, or letters from your physician documenting your current health status. Providing these upfront can sometimes eliminate the need for formal APS requests.

For complicated medical histories, consider having your physician write a brief letter summarizing your current health status, treatment compliance, and prognosis. A clear, concise summary from your doctor can significantly influence underwriting decisions.

The Driving Record Consideration

Many applicants don’t realize that motor vehicle records factor into life insurance underwriting. Multiple speeding tickets, DUI/DWI offenses, or accidents can result in rate increases or even declination, as they’re viewed as indicators of risk-taking behavior.

If you have driving violations, understanding each carrier’s specific policies can guide you toward insurers more lenient on motor vehicle issues. Some carriers don’t penalize a single speeding ticket, while others impose surcharges. DUI/DWI offenses typically require 5-7 years from completion of all requirements (including probation) before standard rates are available, though some carriers are more flexible than others.

Strategy 11: Leverage the Guaranteed Issue and Simplified Issue Alternatives Strategically

The final strategy for securing affordable term life insurance involves understanding when to utilize guaranteed issue or simplified issue policies—products that seem contrary to our goal of premium optimization but can actually save money in specific situations.

Understanding Simplified and Guaranteed Issue Products

Simplified issue policies require no medical exam but include health questions on the application. They use accelerated underwriting algorithms, prescription databases, and other data sources to assess risk. Approval is typically within days rather than weeks.

Guaranteed issue policies require no medical exam and no health questions—approval is guaranteed regardless of health status. These are typically available only in smaller amounts ($25,000-$50,000) and have much higher premiums.

At first glance, these seem like expensive options to avoid. However, several scenarios exist where they provide unique value.

When Simplified Issue Makes Strategic Sense

Time-Sensitive Coverage Needs:

If you need coverage immediately—perhaps you’re closing on a house and your mortgage lender requires insurance, or you’re starting a business partnership requiring key person coverage—simplified issue can provide coverage in 24-48 hours while you simultaneously apply for fully underwritten coverage to replace it later.

Medical Exam Anxiety or Scheduling Difficulties:

Some applicants struggle with medical exam scheduling due to work travel, unusual schedules, or anxiety about medical procedures. Simplified issue eliminates this barrier while still providing competitive rates for healthy individuals.

Supplementing Employer Coverage During Job Transitions:

When changing jobs, simplified issue can bridge the gap between losing employer coverage and securing new individual coverage, ensuring continuous protection without the pressure of rushing medical exams during a stressful transition.

Recent Health Improvements:

If you’ve recently improved your health significantly but don’t yet have enough history to prove it through traditional underwriting, simplified issue algorithms sometimes weight current prescription patterns and recent data more heavily than longer-term history.

The Simplified Issue Rate Comparison

For healthy applicants, simplified issue rates are typically 15-30% higher than fully underwritten policies. However, for those with minor health issues that complicate traditional underwriting, simplified issue can occasionally produce better rates because the algorithms handle certain conditions more favorably than human underwriters.

Example Scenario:

Patricia, a 47-year-old with well-controlled hypothyroidism and borderline high cholesterol, received a Standard Plus classification through traditional underwriting at $78 monthly for $500,000 coverage. Out of curiosity, she also applied through a simplified issue product that used algorithmic underwriting.

The simplified issue product, analyzing her prescription compliance, recent lab work, and other data points, offered Preferred classification at $71 monthly—$7 less per month despite no medical exam. The algorithm viewed her consistent medication compliance and stable lab trends more favorably than the human underwriter who focused on her absolute cholesterol numbers.

While this favorable outcome isn’t guaranteed, it illustrates that simplified issue deserves consideration even for applicants who qualify for traditional coverage.

The Guaranteed Issue Strategic Use

Guaranteed issue seems impossible to justify from a value perspective—premiums are often 3-5x higher than traditional policies. However, two scenarios warrant consideration:

Uninsurable Through Traditional Underwriting:

For individuals with serious health conditions who cannot qualify for traditional coverage at any price, guaranteed issue provides the only option to leave some death benefit for loved ones. While expensive, having $25,000-$50,000 to cover final expenses and leave a small legacy may justify the premium.

Immediate Small-Amount Needs:

For specific purposes requiring immediate, modest coverage—perhaps covering a small business loan or providing funds for final expenses—guaranteed issue can serve the need when time doesn’t allow traditional underwriting.

The Hybrid Strategy:

Some families use a combination approach: purchase guaranteed or simplified issue immediately for baseline protection, simultaneously apply for fully underwritten coverage, and replace the expensive policy once the better coverage is approved. This ensures continuous protection while optimizing costs.

Implementing Your Term Life Insurance Strategy: A Practical Action Plan

Now that we’ve covered eleven powerful strategies for securing the best term life insurance policies in 2026, let’s discuss implementation. Knowledge without action produces no results, and the compound effect of delaying even a few months can cost thousands in unnecessarily higher premiums.

Your 30-Day Implementation Timeline

Days 1-7: Assessment and Preparation

Calculate your actual coverage needs using income replacement, debt coverage, and future expense methods. Review your current health metrics and identify any areas for near-term optimization. Request your prescription history and motor vehicle record to understand what underwriters will see. Research your family health history to accurately complete applications.

Days 8-14: Market Research and Quote Gathering

Identify 3-5 independent brokers or direct carriers to compare. Request comprehensive quotes from multiple carriers through each broker. Ensure you’re comparing identical coverage specifications across all quotes. Research each recommended carrier’s financial strength ratings.

Days 15-21: Application and Optimization

Select your optimal carrier(s) based on total cost, financial strength, and company reputation. If needed, implement the 48-hour pre-exam optimization protocol. Schedule your medical examination at your optimal time window. Complete your application thoroughly and honestly with strategic disclosure.

Days 22-30: Underwriting and Approval

Respond promptly to any underwriter questions or requests. Provide context and documentation proactively to accelerate approval. If the initial offer isn’t optimal, negotiate or request reconsideration with supporting evidence. Once approved, verify all policy details before finalizing.

The Annual Review Commitment

Securing great coverage today doesn’t mean your work is done. Life insurance needs and opportunities evolve, and an annual review ensures your coverage remains optimal.

Annual Review Checklist:

Verify coverage amount still aligns with current needs (has your mortgage balance decreased? have you had additional children? has your income changed significantly?). Assess whether significant health improvements warrant reapplication for better rates. Confirm beneficiary designations remain current. Evaluate whether policy riders or features still provide value. Review payment mode to ensure you’re still using the most economical option.

Common Implementation Pitfalls to Avoid

Even armed with excellent strategies, many families sabotage their own success through predictable mistakes:

Paralysis Through Over-Analysis:

Some people research endlessly without ever applying. Remember, your age increases and health can change—at some point, you need to commit to an application.

Chasing the Absolute Lowest Price:

The cheapest quote isn’t always the best value if it comes from a financially weaker carrier or includes hidden limitations. Balance price with quality and security.

Ignoring the Beneficiary Designation:

Your policy is worthless if you don’t complete beneficiary designations properly. Include both primary and contingent beneficiaries, use specific names rather than generic designations like “my children,” and review these designations whenever your family situation changes.

Letting Policies Lapse:

Set up automatic payments and maintain sufficient funds to avoid accidental lapses. Most policies have a 30-day grace period, but why risk it?

Forgetting About the Policy:

Keep policy documents accessible and ensure family members know coverage exists and how to file a claim. An unknown policy provides no benefit.

The Future of Term Life Insurance: What’s Coming in 2026 and Beyond

As we look at the landscape of best term life insurance products, several emerging trends are worth noting for families planning their coverage strategy.

Accelerated Underwriting Evolution

The movement toward accelerated underwriting using big data, predictive analytics, and machine learning continues expanding. By late 2026, industry experts predict that over 60% of healthy applicants will be able to secure coverage without traditional medical exams through sophisticated algorithmic underwriting.

This creates opportunities and challenges. For healthy individuals with predictable profiles, accelerated underwriting provides faster approval and competitive rates. However, for those with complex health histories, traditional underwriting with human oversight may still produce better outcomes.

Wearable Device Integration

Several carriers are experimenting with programs that integrate wearable fitness device data into underwriting or offer premium discounts for healthy behaviors tracked through wearables. While still limited, this trend may expand significantly over the next few years.

The implications for consumers are mixed—while wellness programs can reduce premiums for the health-conscious, they also raise privacy considerations about sharing continuous health and behavior data with insurance companies.

Policy Customization and Flexibility

The rigid term structures of the past are giving way to more flexible products. Some carriers now offer adjustable term lengths, coverage amount modification options without new underwriting, and enhanced conversion features that provide more options for transitioning to permanent coverage.

These innovations typically come at modest premium increases but provide valuable optionality for families whose circumstances may change unpredictably.

Conclusion: Taking Control of Your Family’s Financial Protection

The difference between families who secure the best term life insurance at affordable term life insurance rates and those who overpay by thousands comes down to knowledge and action. The eleven strategies we’ve covered—optimal timing, health classification optimization, bundling advantages, payment mode selection, rider evaluation, medical exam preparation, comprehensive comparison shopping, ladder structuring, application sequencing, underwriting process management, and strategic use of simplified issue products—represent the insider knowledge that the insurance industry doesn’t advertise but that makes all the difference in real-world premium costs.

Consider this: a family implementing even five of these eleven strategies could realistically reduce their life insurance costs by 30-50% compared to accepting the first quote from a single carrier without optimization. Over a 20-year term on a $1 million policy, this translates to $15,000-$25,000 in savings—money that could fund college education, accelerate mortgage payoff, or bolster retirement security.

The stakes are too high and the savings too substantial to approach this decision passively. Your family’s financial protection deserves the same research and strategic thinking you’d apply to purchasing a home, selecting investments, or planning retirement.

Start today. Calculate your needs, optimize your health metrics, compare multiple carriers, and secure coverage while you’re young and healthy. Every month you delay potentially costs hundreds or thousands in lifetime premiums. The cheapest term life insurance for families in 2026 is the policy you purchase today at the best possible rate, not the one you’ll wish you’d bought when reviewing your costs five years from now.

Your family’s future financial security depends on the decisions you make today. Make them count.

Frequently Asked Questions About Best Term Life Insurance

Q: How much term life insurance coverage do I actually need?

A: The standard recommendation is 10-12 times your annual income, but this oversimplifies your actual needs. A more accurate calculation considers your outstanding debts (mortgage, car loans, student loans), income replacement for your dependents (typically 5-10 years of your income), future expenses like college funding, and final expense coverage. For most families, this results in coverage between $500,000 and $2 million. Online calculators can provide personalized estimates, but consider consulting with a financial advisor for complex situations.

Q: What’s the difference between term and whole life insurance, and why is term usually recommended?

A: Term life insurance provides coverage for a specified period (10, 20, or 30 years) and pays a death benefit only if you die during that term. Whole life provides lifetime coverage and includes a cash value component that grows over time. For most families, term insurance is recommended because it provides substantially more coverage per premium dollar—often 8-10 times more. Unless you have specific estate planning needs, permanent insurance needs, or have already maxed out all other investment vehicles, term insurance provides better value for pure protection needs.

Q: Can I get life insurance if I have pre-existing health conditions?

A: Yes, though your options and rates depend on the specific condition and how well it’s controlled. Conditions like well-managed high blood pressure, controlled diabetes, treated thyroid issues, or past cancer in remission don’t automatically disqualify you. Working with an independent broker who knows which carriers specialize in your specific condition can help you find the best rates. For serious health conditions, guaranteed issue policies ensure you can get some coverage even if traditional underwriting would decline you.

Q: Should I buy term life insurance through my employer or purchase an individual policy?

A: Generally, purchasing an individual policy provides better value and security. While employer coverage offers convenience and guaranteed issue, it typically costs 30-200% more than individual policies when you account for the true cost. More importantly, employer coverage isn’t portable—you lose it when changing jobs or retiring, often when replacement becomes expensive or impossible due to age or health changes. The best strategy is owning an individual policy you control and treating any employer-provided coverage as a supplement.

Q: How do I know if I’m getting the best rate for my health and age?

A: The only way to know with certainty is comparing quotes from multiple carriers—at least 5-7 if possible. Rates can vary by 40-60% for identical coverage based on each carrier’s underwriting philosophy and risk appetite. Work with independent brokers who represent many carriers, use online comparison tools from multiple sources, and don’t assume the first quote you receive is competitive. Request written illustrations showing identical coverage specifications to ensure accurate comparisons.

Q: What happens if I outlive my term life insurance policy?

A: When your term ends, your coverage simply expires with no payout or return of premiums (unless you purchased a return-of-premium rider). This is actually the desired outcome—it means you survived the period when your family needed the protection most. At term end, you typically have several options: let it lapse if you no longer need coverage, convert it to permanent insurance without new medical underwriting (if your policy includes conversion options), or apply for new coverage (though rates will be significantly higher due to your age).

Q: How long does the application and approval process typically take?

A: For traditional fully underwritten policies, expect 4-8 weeks from application to final approval. This includes time for the medical exam (typically scheduled within 1-2 weeks of application), laboratory analysis (3-5 days), underwriting review (1-3 weeks), and any additional requirements like attending physician statements (which can add 2-4 weeks). Accelerated or simplified issue policies can provide approval in 24-48 hours. You can expedite the process by responding promptly to underwriter requests and proactively providing documentation.

Q: Can I have multiple term life insurance policies from different companies?

A: Absolutely, and the ladder strategy we discussed specifically uses multiple policies to optimize coverage and costs. There’s no prohibition on having policies from different carriers, and in fact, this strategy often produces the best overall value. Each policy is underwritten independently (though all applications are reported to the Medical Information Bureau). Just ensure your total coverage amount is reasonable relative to your income and insurable interest—carriers may question applications for coverage dramatically exceeding your financial justification.