INTRODUCTION:

Universal Life Insurance vs Roth IRA: The Introduction That Could Change How You Build Wealth

If you’ve ever sat across from a financial advisor, scrolled through personal finance blogs late at night, or watched a retirement planning video on YouTube, chances are you’ve encountered the heated debate around Universal Life Insurance vs Roth IRA. It’s one of those topics that sparks strong opinions, bold marketing claims, and—unfortunately—costly misunderstandings.

On the surface, the comparison seems straightforward. One is a life insurance policy with a cash value component. The other is a retirement investment account designed for tax-free growth. Simple, right?

Not quite.

Because beneath that surface lies a complex web of tax strategies, long-term projections, fee structures, risk tolerance considerations, estate planning implications, and behavioral finance traps that most people don’t fully grasp until it’s too late.

And here’s the uncomfortable truth: choosing incorrectly—or choosing for the wrong reasons—can quietly cost you tens of thousands of dollars over your lifetime.

That’s not dramatic. That’s math.

Why the Universal Life Insurance vs Roth IRA Debate Matters More Than Ever

We’re living in an era of uncertainty:

- Rising inflation

- Market volatility

- Changing tax laws

- Longer life expectancy

- Unpredictable economic cycles

Retirement planning today isn’t what it was 30 years ago. Traditional pensions have largely disappeared. Social security’s long-term sustainability is frequently questioned. And individuals are now primarily responsible for designing their own financial future.

In that environment, the question becomes urgent:

Where should your money go for maximum long-term advantage?

Should you prioritize a Roth IRA, known for tax-free growth and simplicity? Or should you consider Universal Life Insurance, which promises tax-deferred accumulation, flexible premiums, and a lifetime death benefit?

The confusion grows because both strategies are often marketed as “tax-free retirement solutions.”

But they are not identical. And treating them as interchangeable is one of the most dangerous financial mistakes you can make.

Understanding the Core Difference Early

At its core, this debate comes down to purpose.

A Roth IRA is designed specifically for retirement investing. Contributions are made with after-tax dollars, and qualified withdrawals in retirement are tax-free. According to official Roth IRA guidelines from the IRS, earnings can be withdrawn tax-free after age 59½ and after the five-year holding requirement is met. That clarity and structure make it one of the most powerful retirement tools available.

Universal Life Insurance, on the other hand, is fundamentally a permanent life insurance policy. It provides:

- A death benefit

- A cash value component

- Flexible premium payments

- Potential tax-deferred growth

Depending on the type—fixed, indexed, or variable—your cash value may grow based on interest rates or market performance.

This is where the marketing begins.

You’ll often hear phrases like:

- “Be your own bank.”

- “Tax-free retirement income.”

- “Market gains with downside protection.”

- “Infinite banking strategy.”

And while there are legitimate use cases for Universal Life Insurance, the way it’s often presented can blur the line between protection and investment.

That blur is where mistakes happen.

The Emotional Pull Behind Universal Life Insurance vs Roth IRA

Money decisions are rarely purely logical.

Universal Life Insurance feels safe because it’s tied to insurance. Insurance equals protection. Protection equals security. That psychological framing is powerful.

Roth IRAs, especially when invested in market-based assets, can feel volatile. The word “market” triggers fear in many people. We remember downturns more vividly than growth periods.

But when you look historically at long-term market performance—such as the data tracked by the S&P 500 Index—you’ll see that disciplined, long-term investors have historically been rewarded for staying invested through cycles.

That doesn’t eliminate risk. But it reframes it.

The key issue isn’t whether markets fluctuate. It’s whether you understand what you’re buying and why.

The Cost of Confusion in Wealth Building

One of the biggest problems in the Universal Life Insurance vs Roth IRA discussion is that people often:

- Buy Universal Life when they really need simple investing.

- Avoid Roth IRAs because they misunderstand income limits.

- Overestimate the growth potential of insurance policies.

- Underestimate policy fees and long-term cost structures.

- Treat life insurance as a primary wealth vehicle instead of a supplemental strategy.

And the consequences aren’t immediate.

That’s what makes this dangerous.

In the first few years, everything may look fine. Statements arrive. Cash value grows slowly. Contributions feel manageable.

But over 20–30 years, compounding magnifies structure.

- Fees compound.

- Caps limit gains.

- Policy charges increase with age.

- Investment returns either accelerate or stall wealth accumulation.

Small structural differences become massive financial outcomes.

This Is Not a “One Is Good, One Is Bad” Argument

Let’s be clear about something from the beginning.

This is not an attack on Universal Life Insurance.

And it’s not blind praise for Roth IRAs.

Both can be powerful tools when used correctly.

But both can also be misused when:

- Sold instead of strategically recommended

- Chosen based on marketing instead of math

- Selected without considering income, age, family structure, and long-term goals

The real danger is not in either product itself.

The real danger lies in misunderstanding the role each plays in your financial life.

What This Guide Will Help You Avoid

In the sections that follow, we will examine:

- The structural differences in detail

- The tax implications over time

- The hidden fees most people ignore

- The liquidity differences

- The sequencing strategy many advisors recommend

- The 7 shocking and dangerous wealth-building mistakes people make

Because when it comes to Universal Life Insurance vs Roth IRA, the decision isn’t just about retirement.

It’s about:

- Financial independence

- Generational wealth

- Risk management

- Tax efficiency

- And long-term peace of mind

This isn’t just another comparison article.

It’s a wake-up call to think critically before locking yourself into a strategy that may not align with your true goals.

And by the time you finish reading, you’ll be equipped to make that decision with clarity instead of confusion.

What Is Universal Life Insurance in the Universal Life Insurance vs Roth IRA Debate?

Before we compare, we need clarity.

Universal Life Insurance (UL) is a type of permanent life insurance that includes:

- A death benefit

- A cash value component

- Flexible premium payments

- Adjustable coverage

Unlike whole life insurance, UL policies allow your cash value to grow based on interest rates or market performance (in the case of indexed or variable UL).

The appeal?

- Tax-deferred growth

- Access to cash value through policy loans

- Lifetime coverage

But here’s the nuance many miss:

The cost structure and policy design matter enormously.

If poorly funded or mismanaged, UL can lapse — triggering taxes and eliminating coverage.

What Is a Roth IRA in the Universal Life Insurance vs Roth IRA Conversation?

A Roth IRA is a retirement investment account funded with after-tax dollars.

The benefits?

- Tax-free growth

- Tax-free withdrawals in retirement

- No required minimum distributions (RMDs)

- Broad investment flexibility

According to the IRS Roth IRA guidelines, withdrawals of contributions can be made anytime tax-free, and qualified earnings withdrawals are also tax-free after age 59½ and meeting the 5-year rule.

That’s incredibly powerful.

But there are limitations:

- Annual contribution limits

- Income phase-outs

- No built-in life insurance component

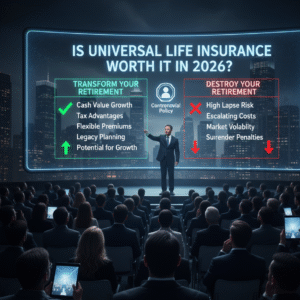

Universal Life Insurance vs Roth IRA Comparison Table

Below is a clear side-by-side breakdown to enhance understanding:

| Feature | Universal Life Insurance | Roth IRA |

|---|---|---|

| Primary Purpose | Life insurance + cash value | Retirement investment |

| Tax Treatment | Tax-deferred growth | Tax-free growth |

| Contributions | Flexible | Annual limits apply |

| Income Limits | None | Income phase-outs |

| Death Benefit | Yes | No |

| Investment Risk | Depends on type (fixed, indexed, variable) | Based on chosen investments |

| Fees | Higher (insurance + policy charges) | Generally lower |

| Liquidity | Policy loans | Contributions anytime |

| Risk of Lapse | Yes | No |

| Best For | High earners, estate planning | Long-term retirement savers |

This table alone reveals something important:

These tools are not identical. They serve different purposes.

Which leads us to the real danger — confusing them.

7 Shocking and Dangerous Wealth-Building Mistakes in the Universal Life Insurance vs Roth IRA Debate

1. Using Universal Life Insurance vs Roth IRA Without Understanding Primary Purpose

The biggest mistake?

Using insurance as an investment substitute.

Universal Life Insurance exists first and foremost to provide a death benefit. The cash value is secondary.

A Roth IRA, on the other hand, is built specifically for retirement investing.

If your primary goal is retirement income and you have no need for permanent insurance, prioritizing UL over a Roth IRA may limit long-term growth due to higher costs.

2. Ignoring the Fee Structure in Universal Life Insurance vs Roth IRA

Universal life policies often include:

- Mortality charges

- Administrative fees

- Cost of insurance adjustments

- Surrender charges

In contrast, many Roth IRA accounts can be opened with low-cost index funds.

For example, broad market funds tracking the S&P 500, such as those following the methodology of the S&P 500 Index, often carry minimal expense ratios.

Fees compound just like returns do — but in reverse.

High internal policy costs can significantly reduce net growth.

3. Overfunding Universal Life Insurance vs Roth IRA Before Maximizing Tax-Advantaged Retirement Accounts

This is a classic sequencing error.

Financial planners often recommend:

- Contribute enough to employer 401(k) to get match

- Max out Roth IRA

- Then explore additional vehicles

Jumping into universal life before maximizing simpler tax-advantaged accounts can be premature.

4. Assuming Universal Life Insurance vs Roth IRA Offers the Same Liquidity

Roth IRA contributions can be withdrawn anytime tax-free.

Universal life loans are technically borrowing against your own policy — and unpaid loans can reduce your death benefit or cause lapse.

Liquidity is not equal.

5. Underestimating Risk in Indexed or Variable UL Policies

Indexed universal life policies often advertise:

- “Market upside with downside protection.”

But caps and participation rates limit gains.

Variable UL carries full market risk.

Unlike Roth IRA investments, where you control asset allocation directly, UL structures add layers of insurance mechanics.

Complexity increases misunderstanding.

6. Ignoring Income Limits in the Universal Life Insurance vs Roth IRA Equation

High earners sometimes cannot contribute directly to a Roth IRA due to income phase-outs.

This is where UL is often marketed aggressively.

But even then, alternatives like backdoor Roth strategies exist.

The point is: income eligibility should be considered carefully before defaulting to insurance-based strategies.

7. Believing Universal Life Insurance vs Roth IRA Is an Either/Or Decision

This may be the most dangerous misconception.

For some high-income earners who:

- Max out retirement accounts

- Need permanent coverage

- Want estate planning flexibility

A properly structured UL policy can complement a Roth IRA.

The debate isn’t binary.

It’s strategic.

Universal Life Insurance vs Roth IRA: Who Should Consider Each?

Roth IRA May Be Better If You:

- Want simple, transparent investing

- Are early in your career

- Don’t need permanent life insurance

- Prefer low-cost index funds

- Value tax-free retirement income

Universal Life Insurance May Be Considered If You:

- Have estate planning needs

- Need permanent life insurance

- Have maxed out retirement vehicles

- Want additional tax-deferred growth

- Understand policy mechanics deeply

The Emotional Side of Universal Life Insurance vs Roth IRA Decisions

Money decisions aren’t purely mathematical.

They’re emotional.

Insurance sales presentations can feel reassuring:

“Tax-free income.”

“Safe growth.”

“Be your own bank.”

Investment platforms can feel intimidating:

“Market volatility.”

“Risk.”

“Long-term compounding.”

But fear-driven decisions rarely lead to optimal outcomes.

You need clarity, not marketing.

Universal Life Insurance vs Roth IRA: The Long-Term Wealth Impact

Let’s think in decades.

A 30-year-old investing $6,500 annually in a Roth IRA earning 8% could accumulate significant tax-free wealth by retirement.

Meanwhile, a UL policy’s early-year cash value growth is often slow due to front-loaded costs.

Time magnifies structure.

And structure determines outcome.

Universal Life Insurance vs Roth IRA Tax Advantages Explained

Roth IRA:

- After-tax contributions

- Tax-free growth

- Tax-free qualified withdrawals

Universal Life:

- Tax-deferred growth

- Tax-free loans (if structured properly)

- Tax-free death benefit

The tax benefits differ in timing and structure.

Understanding when you want tax savings matters more than just hearing the phrase “tax-free.”

Conclusion: Universal Life Insurance vs Roth IRA — Choose Strategy Over Sales

When it comes to Universal Life Insurance vs Roth IRA, the most important realization is this: you are not choosing between two identical wealth-building tools. You are choosing between two fundamentally different financial strategies designed for different primary purposes.

A Roth IRA is a retirement investment vehicle. It is straightforward, transparent, and designed specifically to grow wealth for your future. You contribute after-tax dollars, and in exchange, you receive one of the most powerful benefits in the tax code—tax-free qualified withdrawals. That simplicity is not a weakness. In fact, for many investors, it’s the strength.

Universal Life Insurance, by contrast, is first and foremost life insurance. Yes, it includes a cash value component. Yes, it offers tax-deferred growth. Yes, loans can potentially provide tax-advantaged access to funds. But at its core, it exists to provide a death benefit. The investment component is layered on top of an insurance chassis that comes with internal costs, policy mechanics, and long-term sustainability requirements.

The danger arises when these roles are confused.

If you need retirement growth but buy insurance instead, your money may grow slower due to fees and policy charges. If you need permanent insurance for estate planning but rely solely on a Roth IRA, your family may lack the protection you intended to provide.

The right answer depends on:

- Your income level

- Your current tax bracket versus expected retirement bracket

- Whether you need permanent life insurance

- Whether you have already maxed out retirement accounts

- Your comfort with investment risk

- Your long-term estate planning goals

For many people—especially young earners—the Roth IRA should come first. It’s simple, efficient, and historically effective for long-term compounding.

For high-income earners who have already maxed out retirement vehicles and need permanent coverage, a properly structured Universal Life policy may serve as a complementary strategy—not a replacement.

Remember the seven dangerous mistakes:

- Treating insurance as a primary investment

- Ignoring policy fees

- Skipping foundational retirement accounts

- Misunderstanding liquidity

- Underestimating complexity

- Overlooking income limits

- Framing the decision as either/or instead of strategic sequencing

Wealth-building isn’t about finding a clever product. It’s about building a durable system.

The smartest financial decisions are rarely flashy. They are disciplined. Intentional. Boring, even.

But boring done consistently becomes powerful.

When evaluating Universal Life Insurance vs Roth IRA, slow down. Run projections. Ask better questions. Understand the structure before signing anything.

Because the goal isn’t to win a debate.

The goal is to retire with freedom, security, and confidence in the decisions you made decades earlier.

And that kind of outcome is never accidental.

Frequently Asked Questions: Universal Life Insurance vs Roth IRA

1. Is Universal Life Insurance better than a Roth IRA for retirement?

It depends on your goals.

If your primary objective is retirement income and long-term investment growth, a Roth IRA is often the more straightforward and cost-effective option. It is designed specifically for retirement savings and offers tax-free qualified withdrawals.

Universal Life Insurance may be useful if you need permanent life coverage and have already maximized other tax-advantaged retirement accounts. However, it should rarely replace a Roth IRA as your foundational retirement strategy.

2. Can I lose money in Universal Life Insurance?

Yes, depending on the type of policy.

- Fixed Universal Life offers more predictable growth.

- Indexed Universal Life (IUL) ties returns to a market index, subject to caps and participation rates.

- Variable Universal Life (VUL) allows direct market investment exposure, meaning your cash value can rise or fall.

Additionally, if the policy is underfunded or poorly structured, it can lapse—potentially triggering taxes and eliminating coverage.

3. What are the main tax differences between Universal Life Insurance and a Roth IRA?

Roth IRA:

- Contributions are made with after-tax dollars.

- Qualified withdrawals are tax-free.

- No required minimum distributions (RMDs).

Universal Life Insurance:

- Cash value grows tax-deferred.

- Policy loans may be tax-free if structured properly.

- Death benefit is generally income tax-free.

The difference lies in structure: Roth IRAs offer tax-free growth by design, while Universal Life relies on policy mechanics and loan strategies.

4. Which has higher fees: Universal Life Insurance or Roth IRA?

Generally, Universal Life Insurance has higher internal costs. These may include:

- Cost of insurance charges

- Administrative fees

- Mortality expenses

- Surrender charges

Roth IRAs, especially when invested in low-cost index funds, often have significantly lower expense ratios.

Over decades, fee differences can have a major impact on total accumulated wealth.

5. Can I use both Universal Life Insurance and a Roth IRA?

Absolutely.

For many high-income earners, the most strategic approach is not choosing one over the other—but using them in sequence.

A common order of operations:

- Contribute to employer 401(k) up to the match

- Max out a Roth IRA (if eligible)

- Max out additional retirement vehicles

- Consider Universal Life for supplemental tax-deferred growth and permanent coverage

This layered strategy avoids the mistake of replacing simple, efficient retirement accounts with more complex insurance-based solutions.

6. Is Universal Life Insurance a good “infinite banking” strategy?

It can be—but only when structured correctly and fully understood.

The “infinite banking” concept involves overfunding a policy to build cash value and borrowing against it. However, success depends on:

- Policy design

- Funding level

- Loan management

- Long-term commitment

Without careful structuring, the strategy can underperform expectations.

7. What is the biggest mistake people make in the Universal Life Insurance vs Roth IRA debate?

The biggest mistake is misunderstanding purpose.

When insurance is treated like an investment replacement—or when retirement accounts are ignored in favor of complex policy structures—long-term compounding suffers.

Clarity about your goals should always come before product selection.

Because in the end, it’s not about which tool sounds better.

It’s about which one truly fits your financial life.